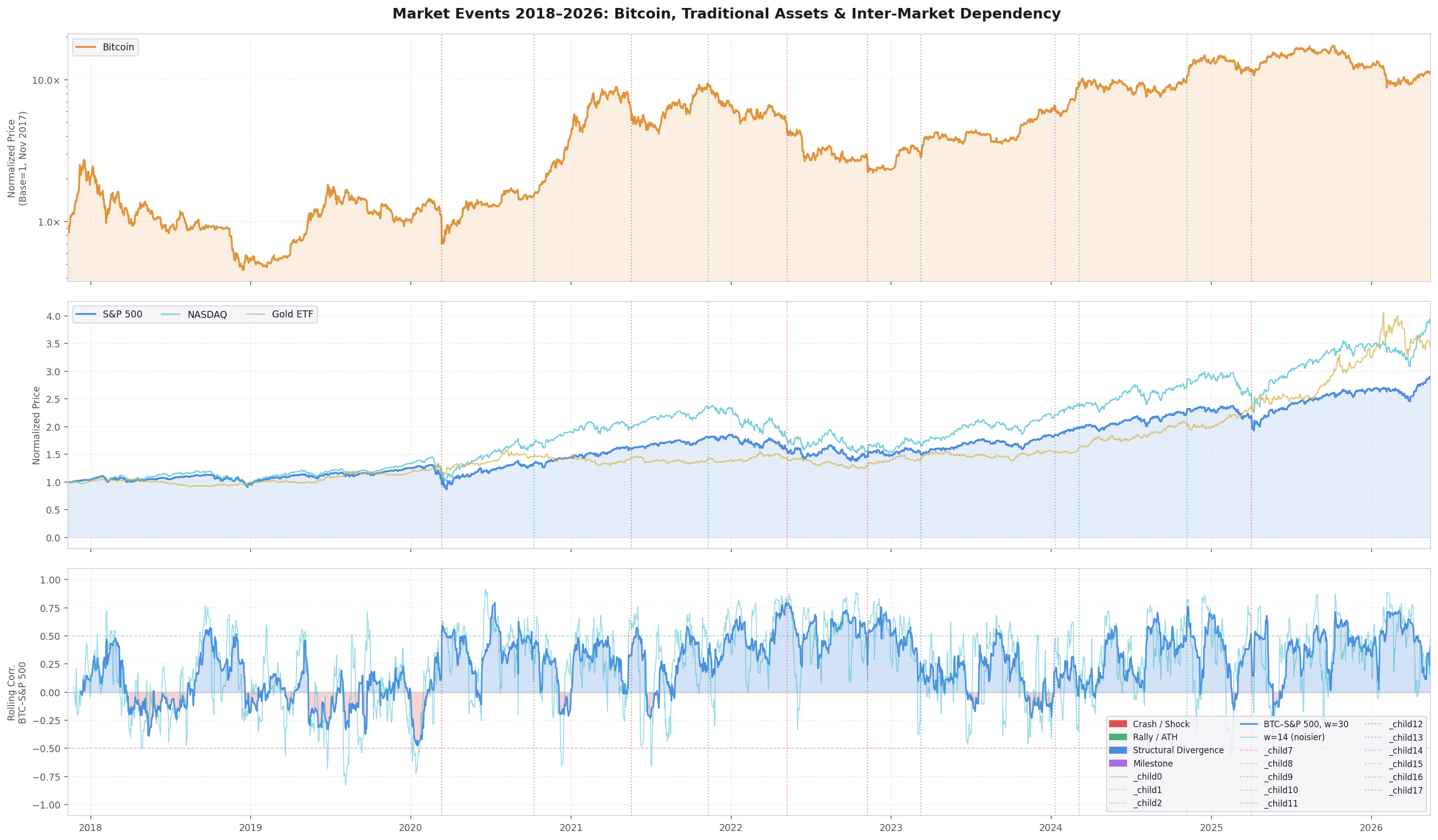

Dataset & Asset Universe

Asset Universe — Detailed

Base asset. World's largest cryptocurrency by market cap. Trades 24/7 including weekends. Serves as the primary source of crypto-derived features throughout the thesis.

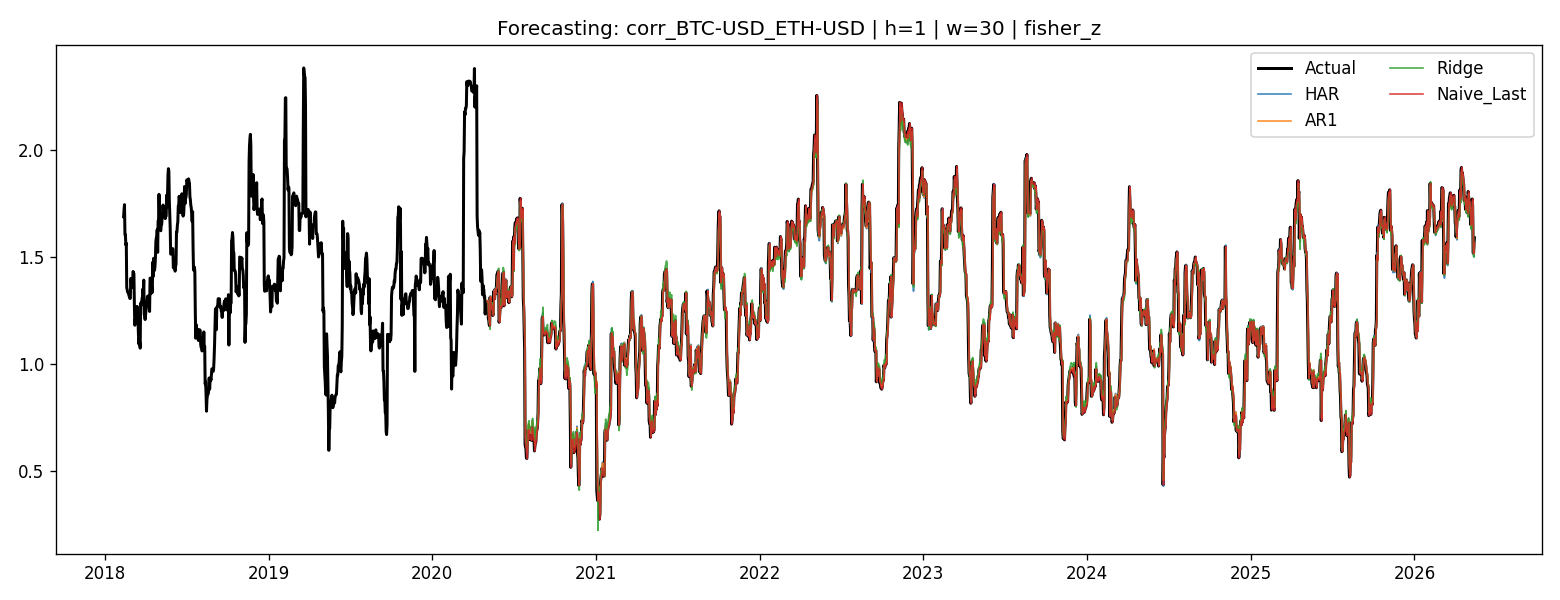

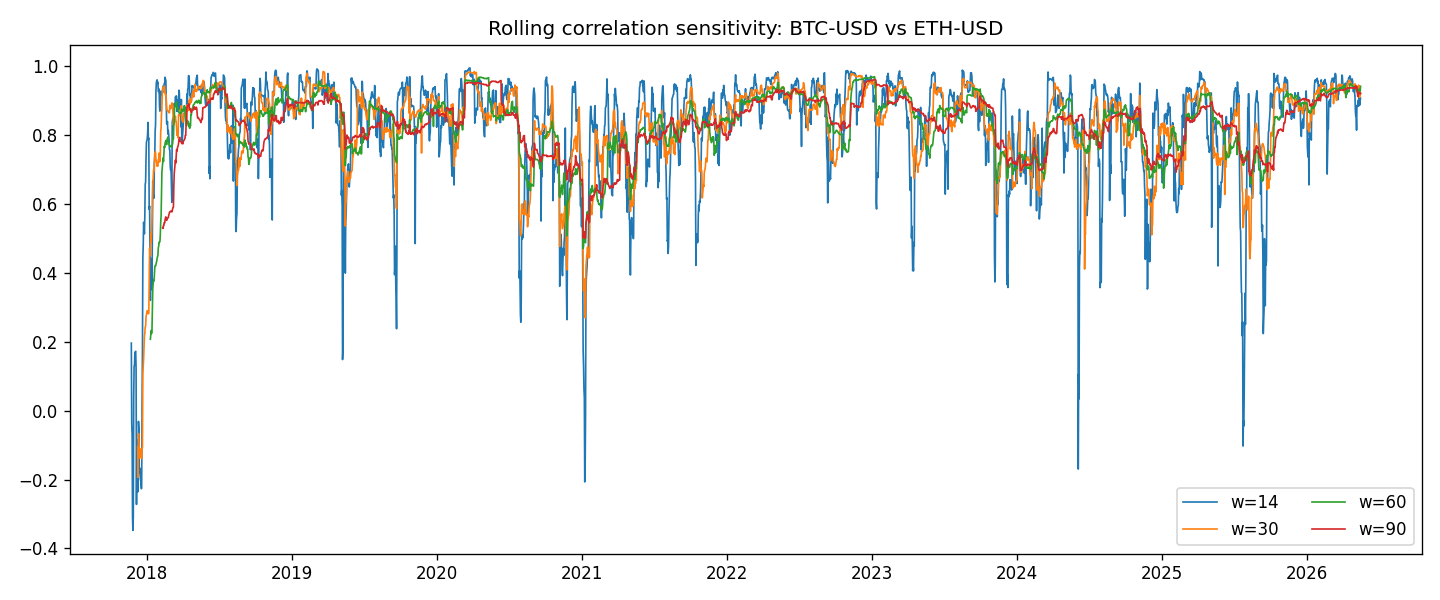

Crypto reference asset. Included to contrast cross-crypto dependency (BTC↔ETH) with crypto-to-conventional dependency. Start date of sample determined by ETH availability on Yahoo Finance.

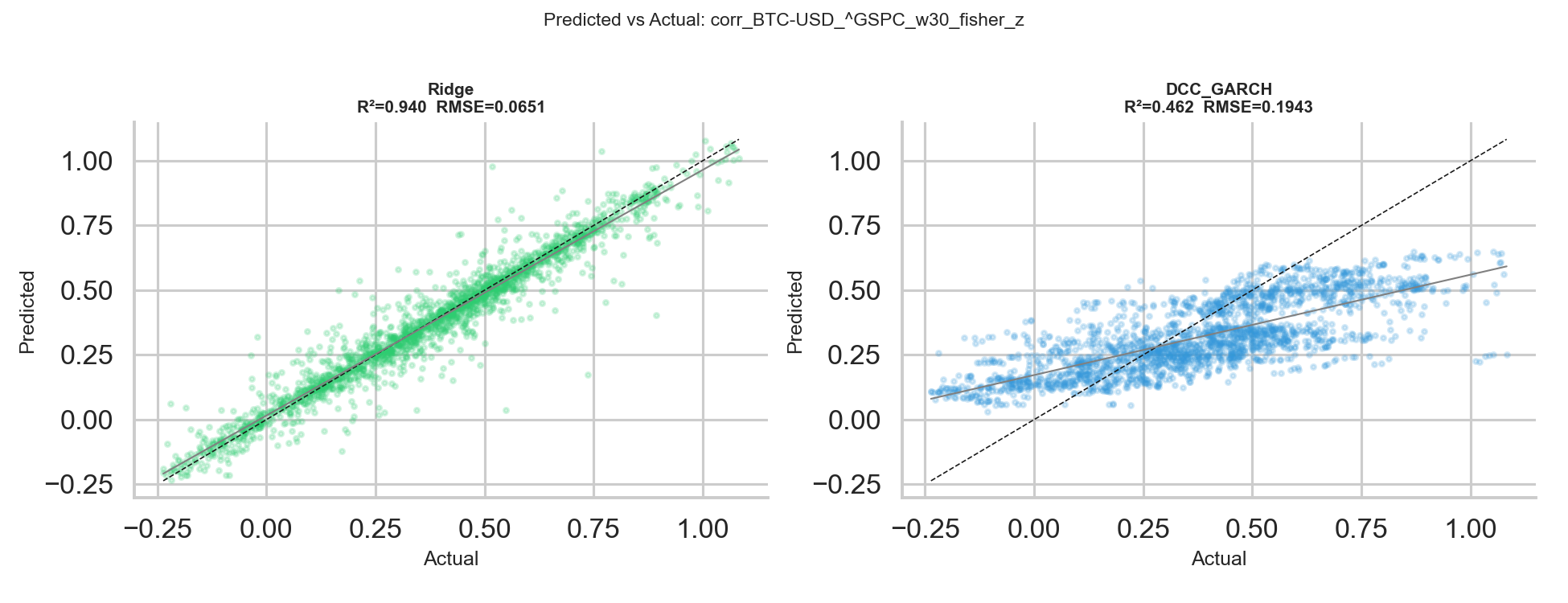

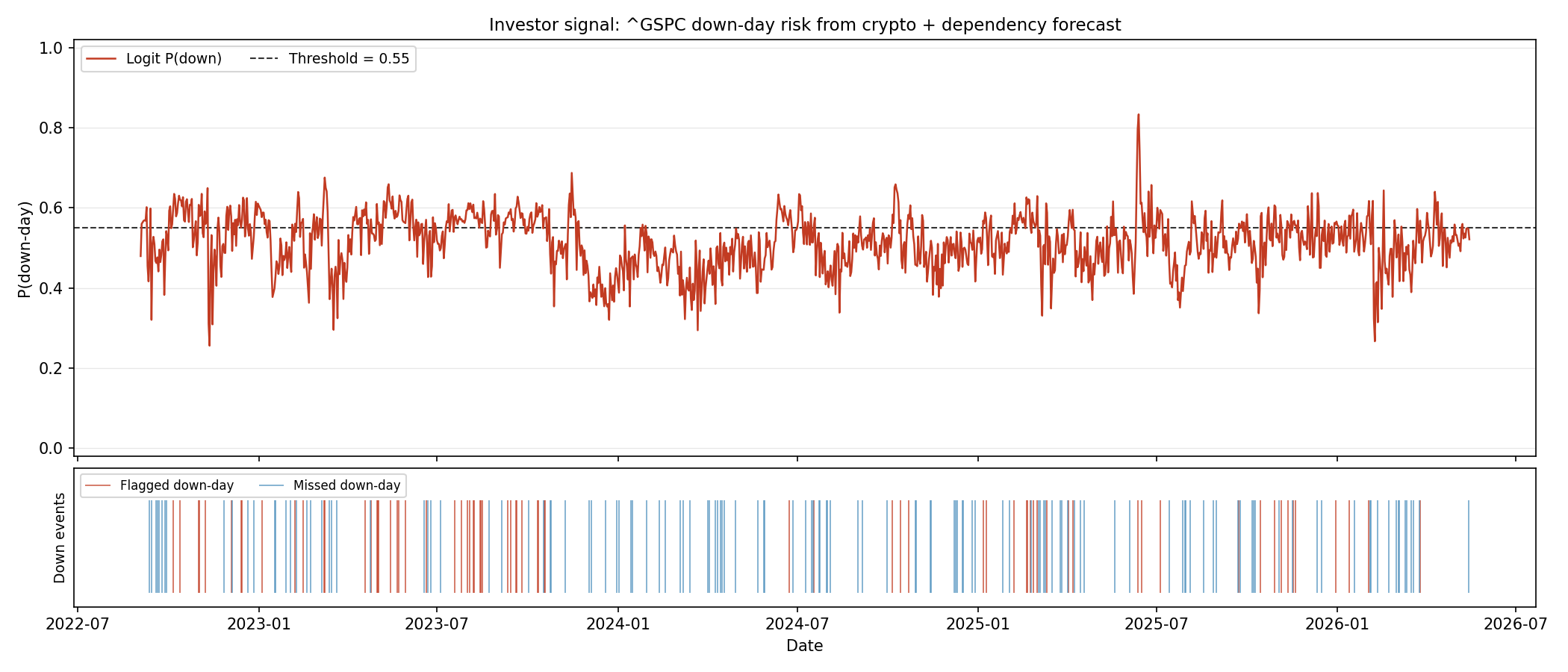

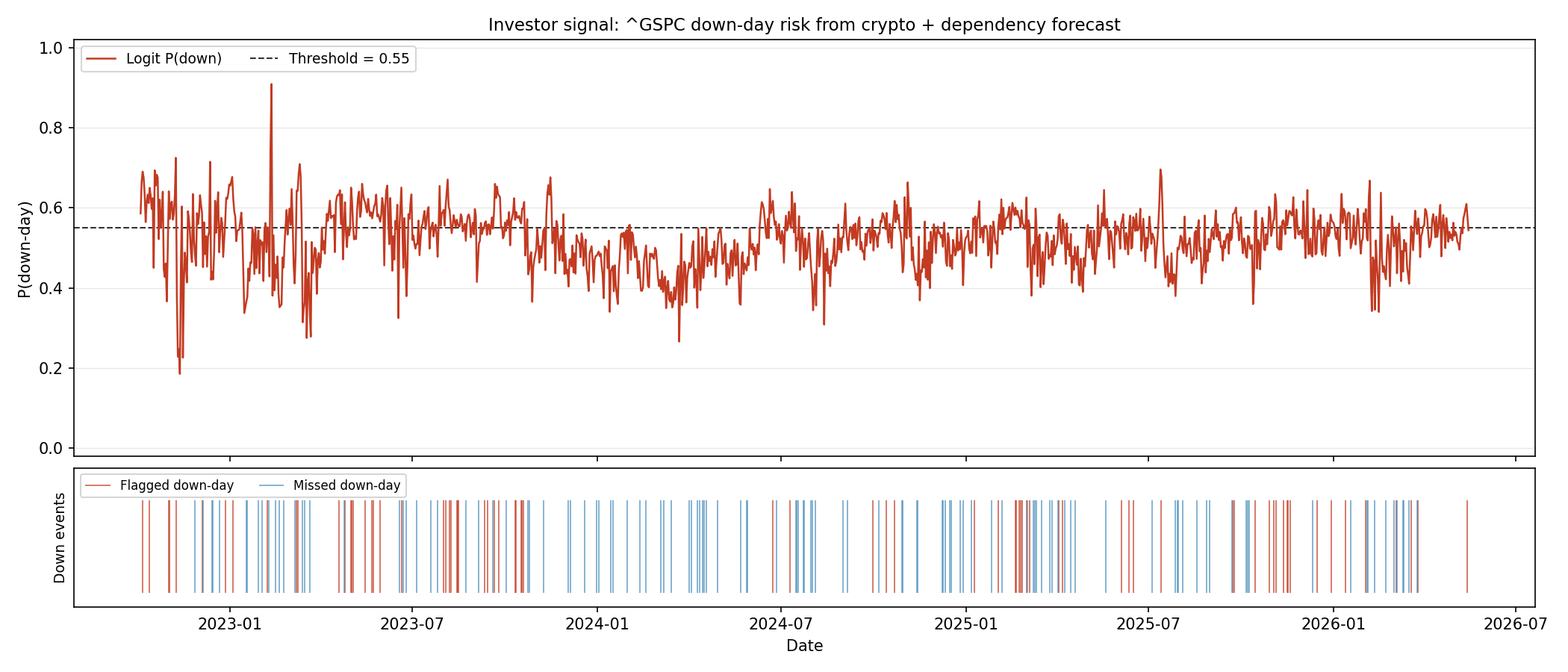

Broad U.S. equity benchmark. Represents large-cap risk appetite; most tightly linked to global funding conditions and sentiment — the same macro forces that drive Bitcoin.

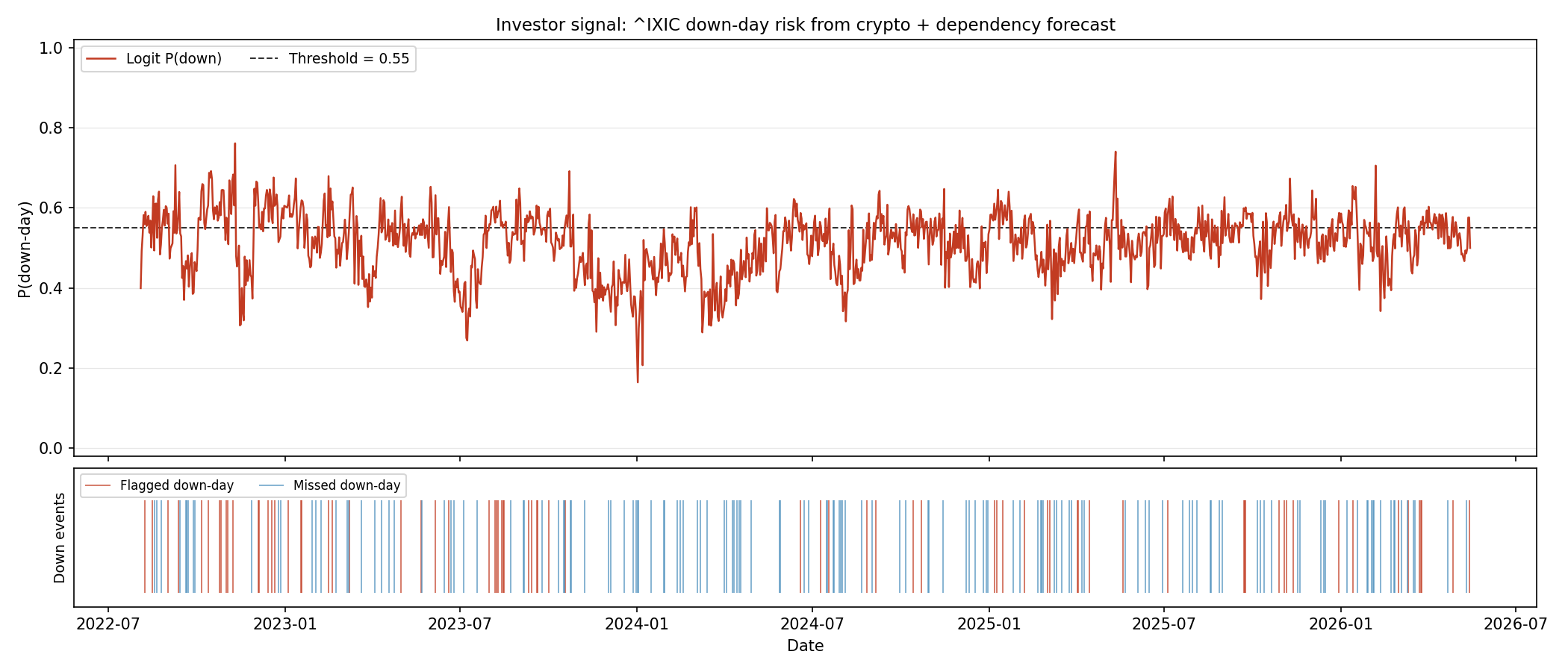

Tech-heavy equity index. Higher beta to growth and speculative sentiment than S&P 500, making it a natural comparator for crypto co-movement.

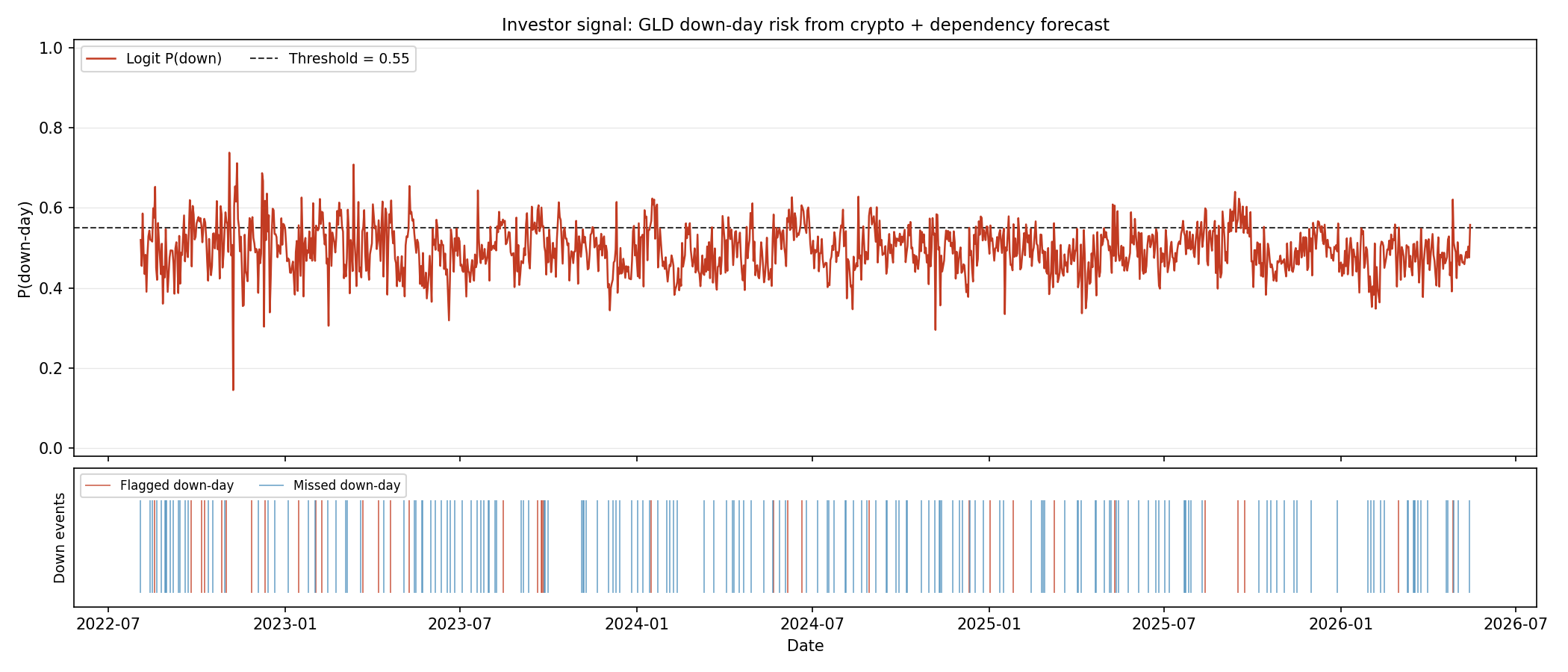

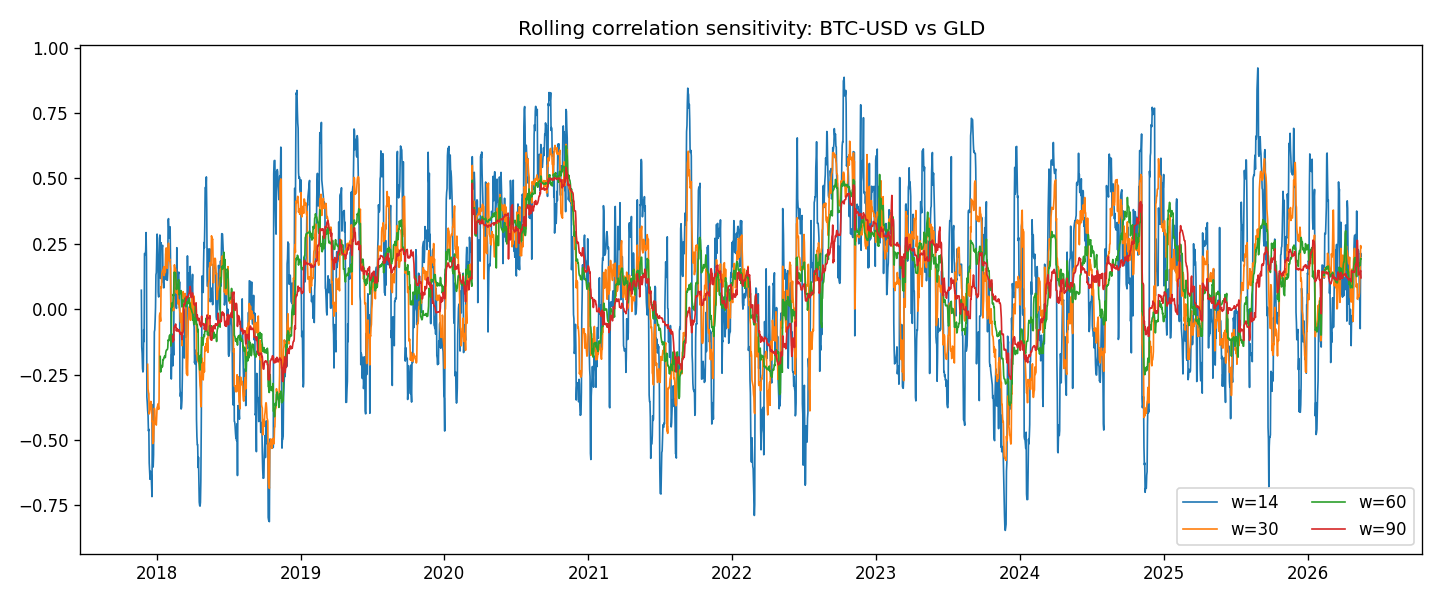

Largest gold ETF. Captures safe-haven demand, inflation expectations, and real interest rate dynamics — structural drivers distinct from crypto.

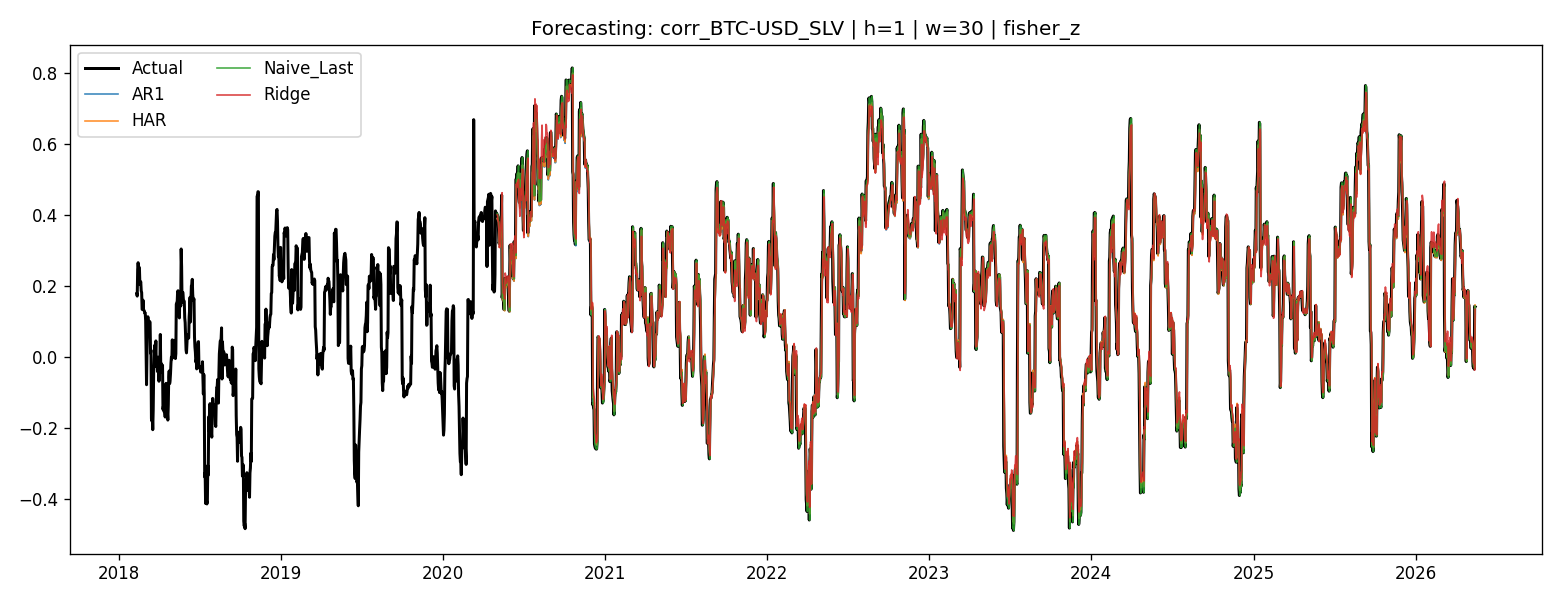

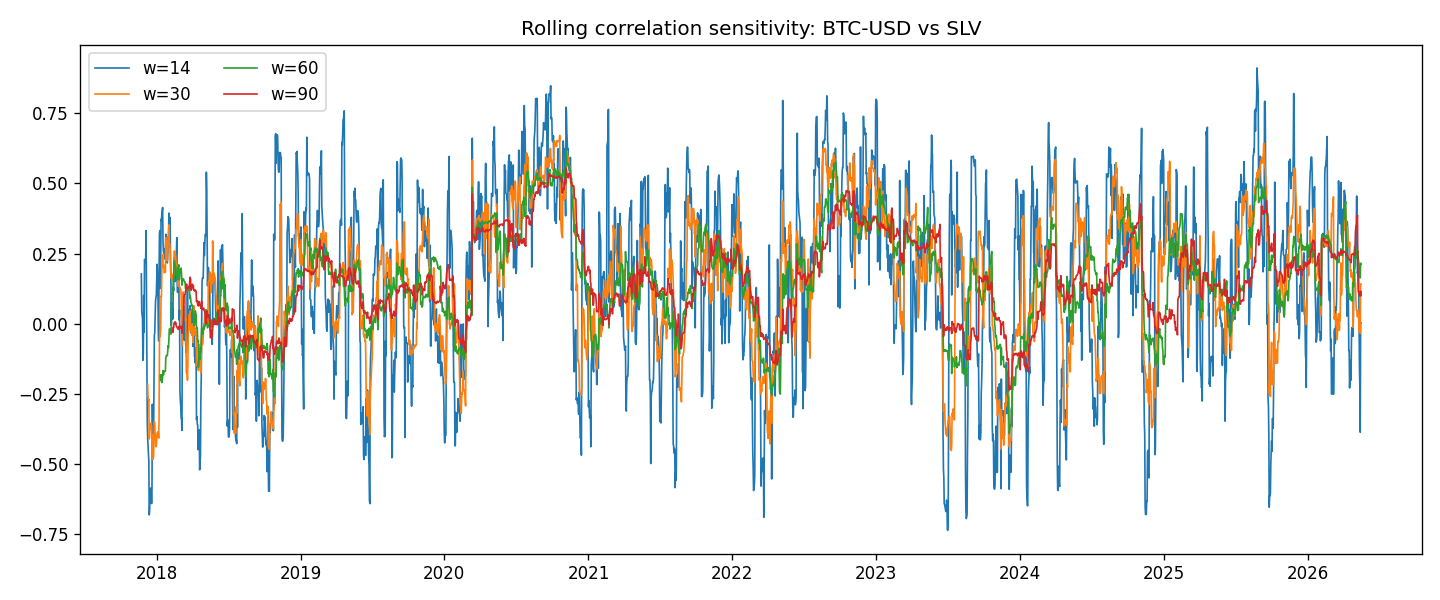

Silver has both safe-haven and industrial demand components. Higher volatility than gold; provides an additional precious-metal data point.

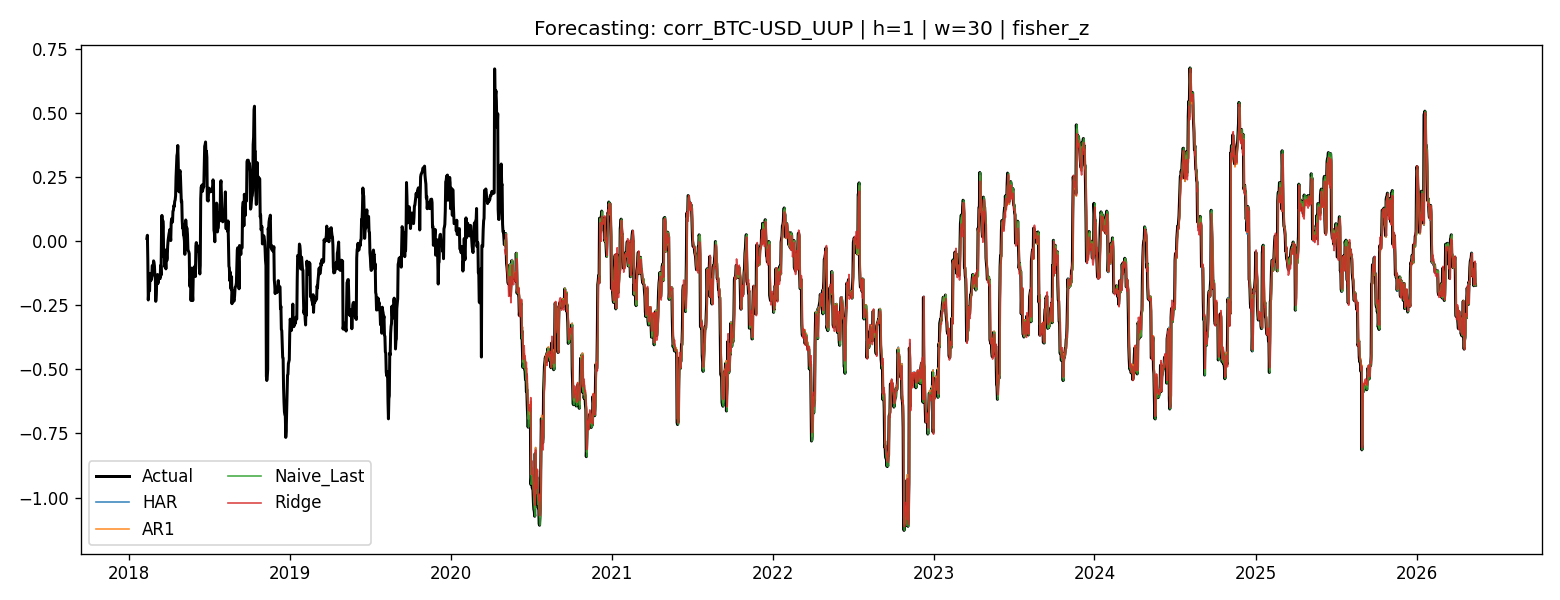

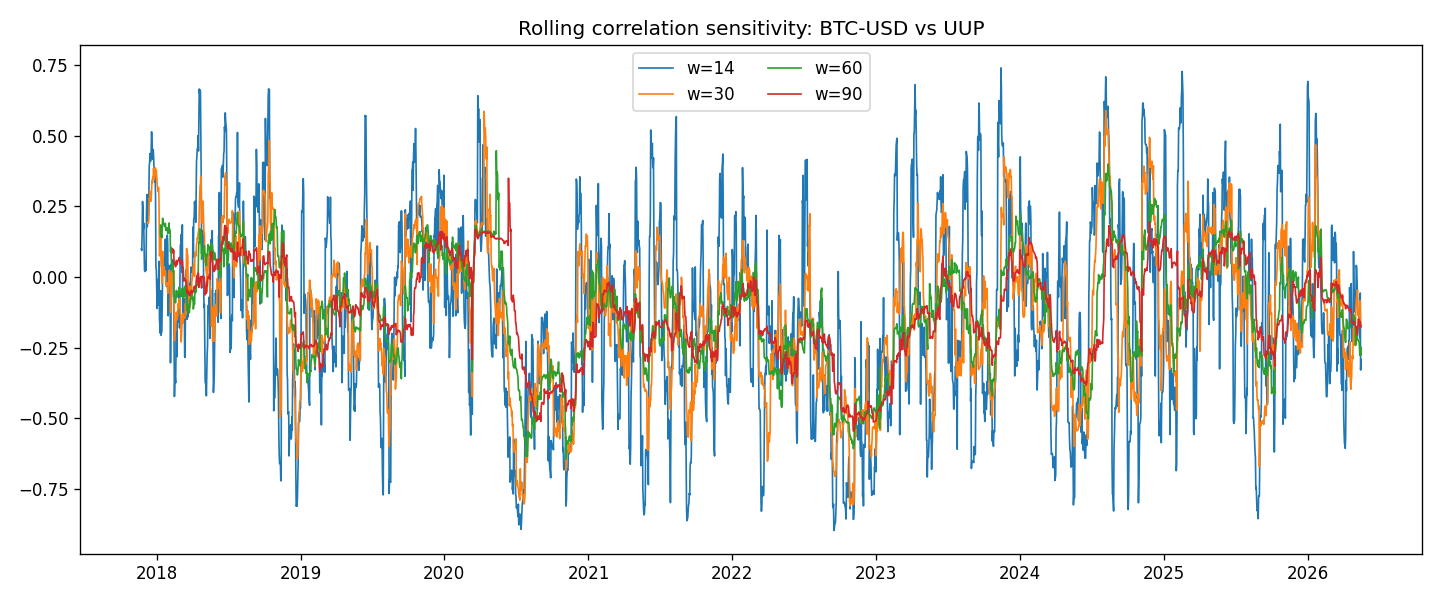

Proxy for broad USD strength (DXY). Reflects global risk-off positioning and macro defensive flows. Responds to geopolitical risk premia not captured by crypto features.

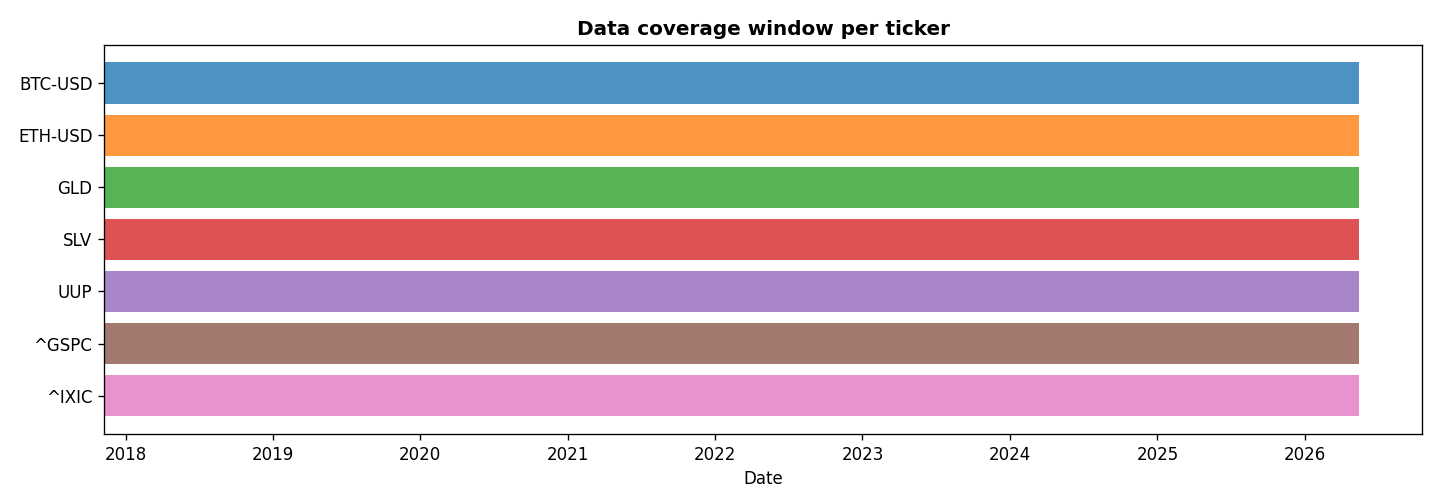

Sample Construction & Alignment

Period: 9 Nov 2017 — 16 May 2026 · 3,053 trading days per asset. Start date is set by the earliest available ETH-USD quote on Yahoo Finance. Earlier dates contain no Ethereum observations and are excluded.

Alignment: Bitcoin and Ethereum trade continuously, including weekends. The panel is built on Bitcoin's seven-day calendar, and the conventional assets — which trade only on business days — are forward-filled across weekends and holidays. Every weekend or holiday row therefore records a zero return for the conventional series (≈900–1000 such days each), while the crypto series are unaffected; all seven tickers share an identical date index. This calendar mismatch is examined as a robustness check in the thesis.

Returns: Log-returns rt = log Pt − log Pt−1 are used throughout. Log-returns are additive over time, approximately normal at moderate horizons, and standard in both econometric modelling and ML pipelines for financial time series.

Data Quality Summary

| Ticker | N obs | % Miss. | Skew | Ex.Kurt | Ann.Vol% |

|---|---|---|---|---|---|

| BTC-USD | 3,053 | 0.00 | −0.73 | 13.38 | 56.08 |

| ETH-USD | 3,053 | 0.00 | −0.74 | 10.77 | 72.68 |

| GLD | 3,053 | 0.00 | −0.89 | 13.96 | 13.82 |

| SLV | 3,053 | 0.00 | −2.77 | 51.61 | 28.20 |

| UUP | 3,053 | 0.00 | −0.03 | 8.58 | 5.85 |

| ^GSPC | 3,053 | 0.00 | −0.73 | 22.59 | 16.20 |

| ^IXIC | 3,053 | 0.00 | −0.46 | 12.65 | 19.66 |

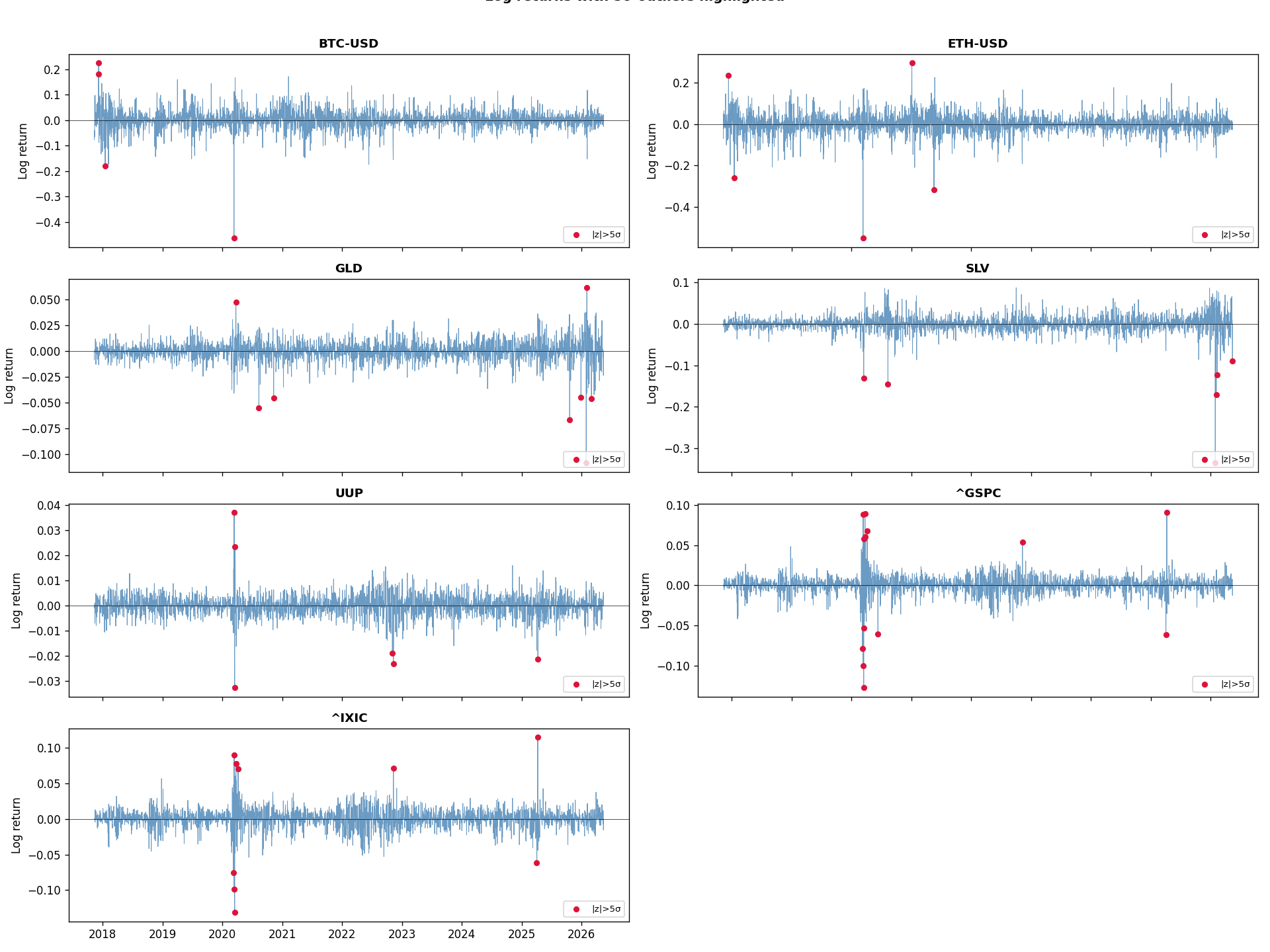

Zero missing values across all tickers after alignment. Crypto assets show substantially higher annualised volatility (56–73% vs 6–28% for conventional assets) and fat tails (excess kurtosis >10).

Walk-Forward Split

(min 800 obs)

~5 years

(~1 calendar month)

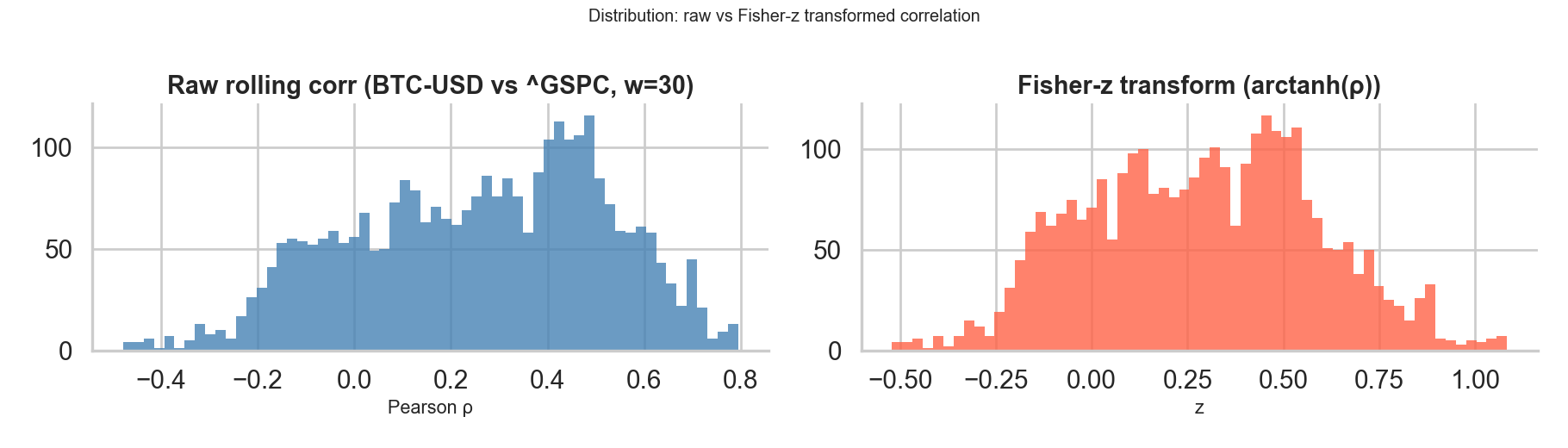

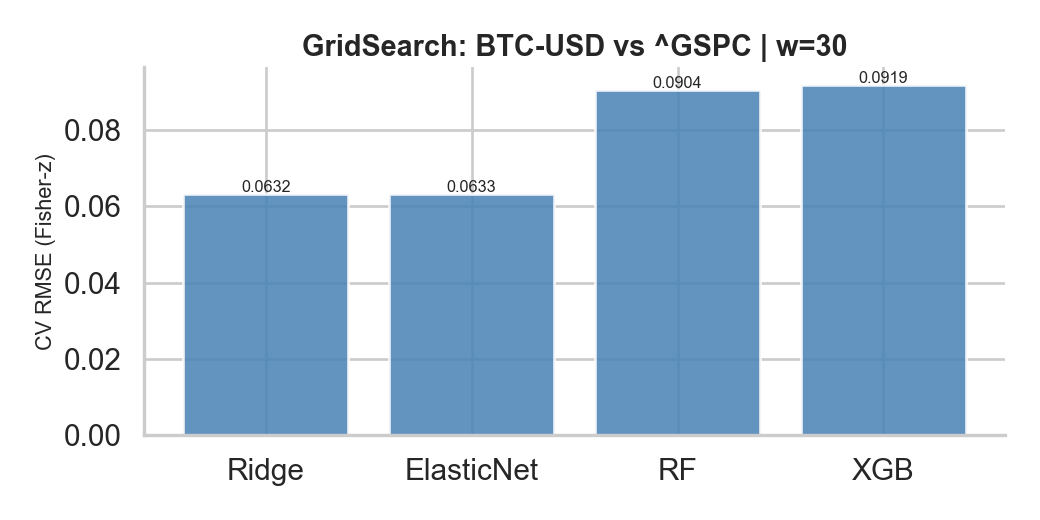

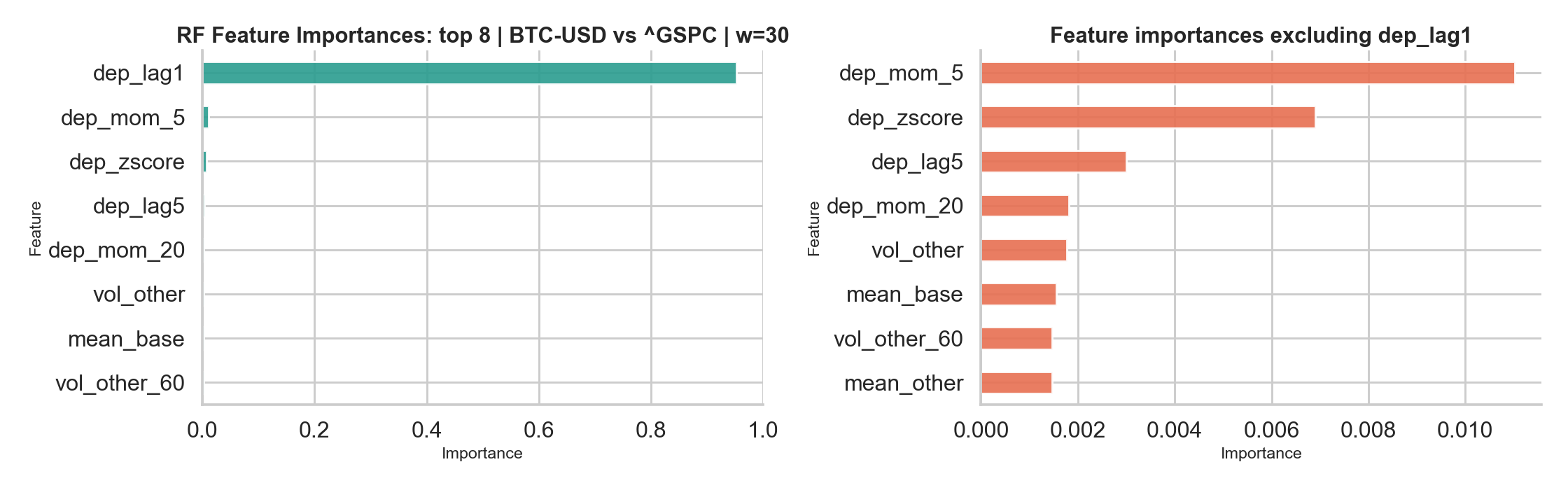

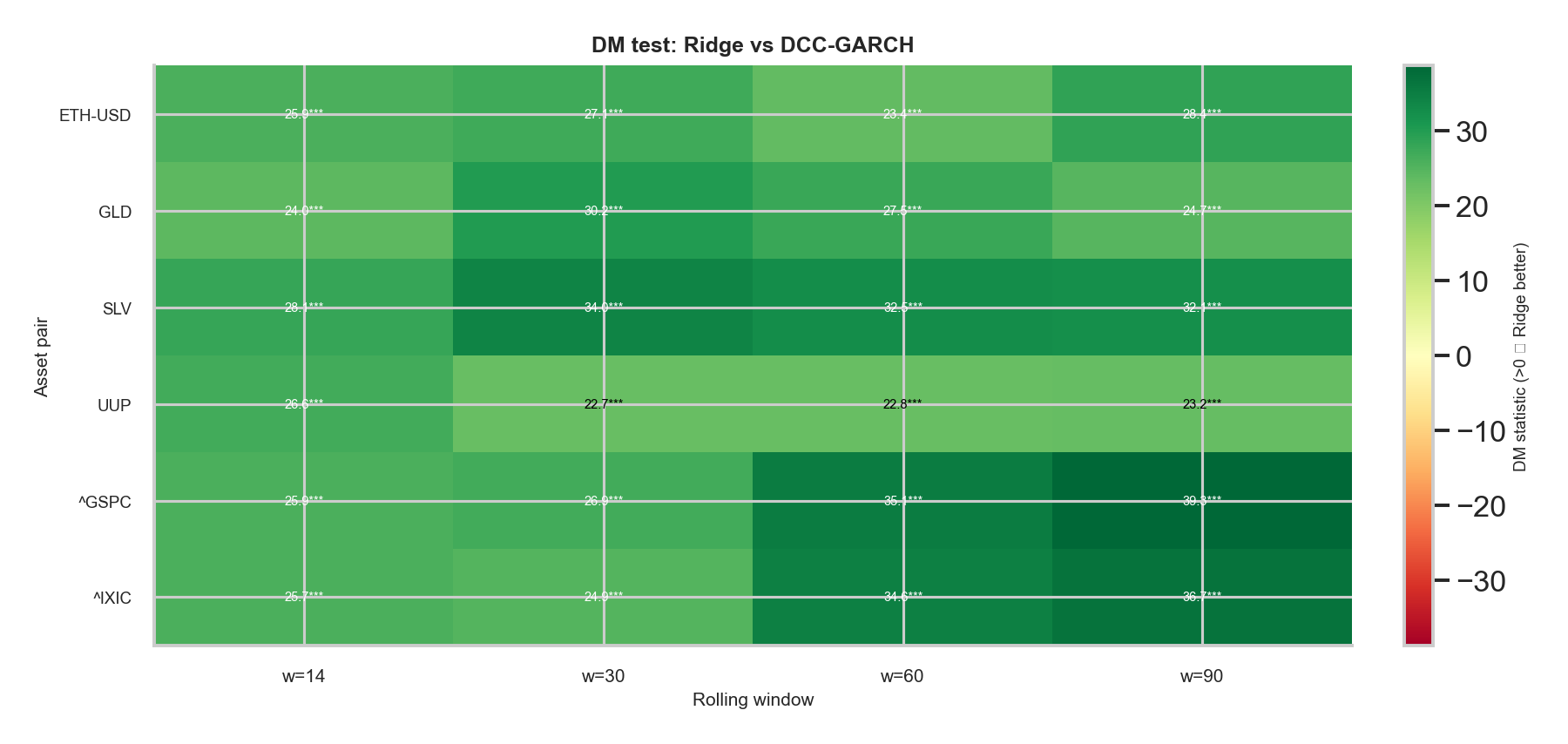

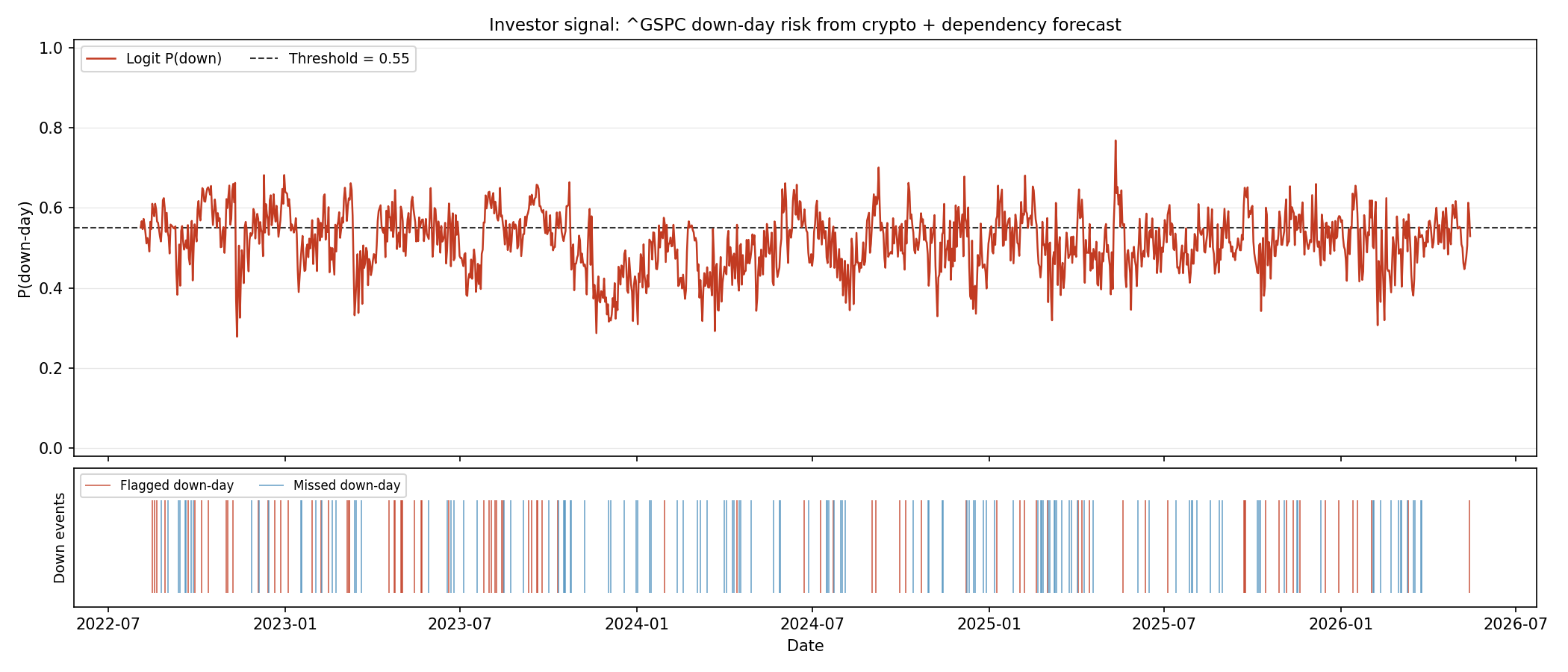

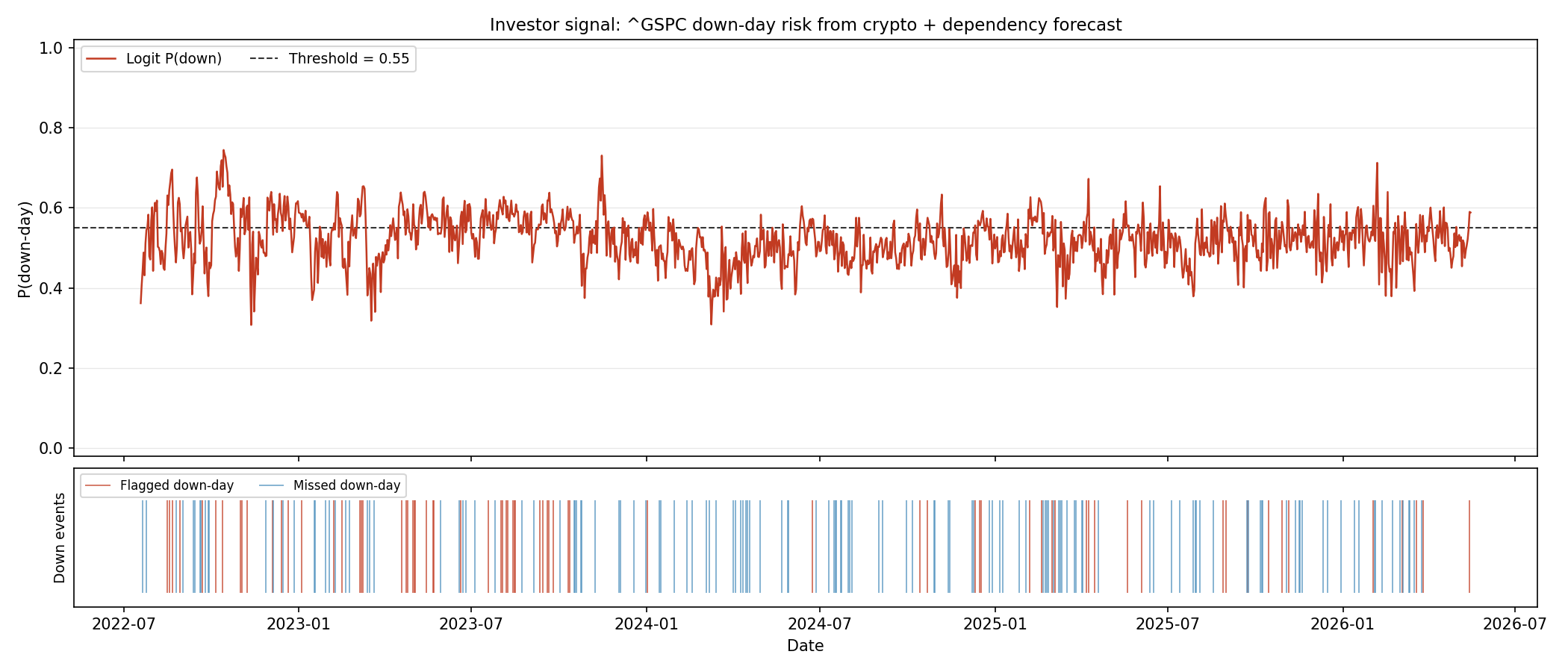

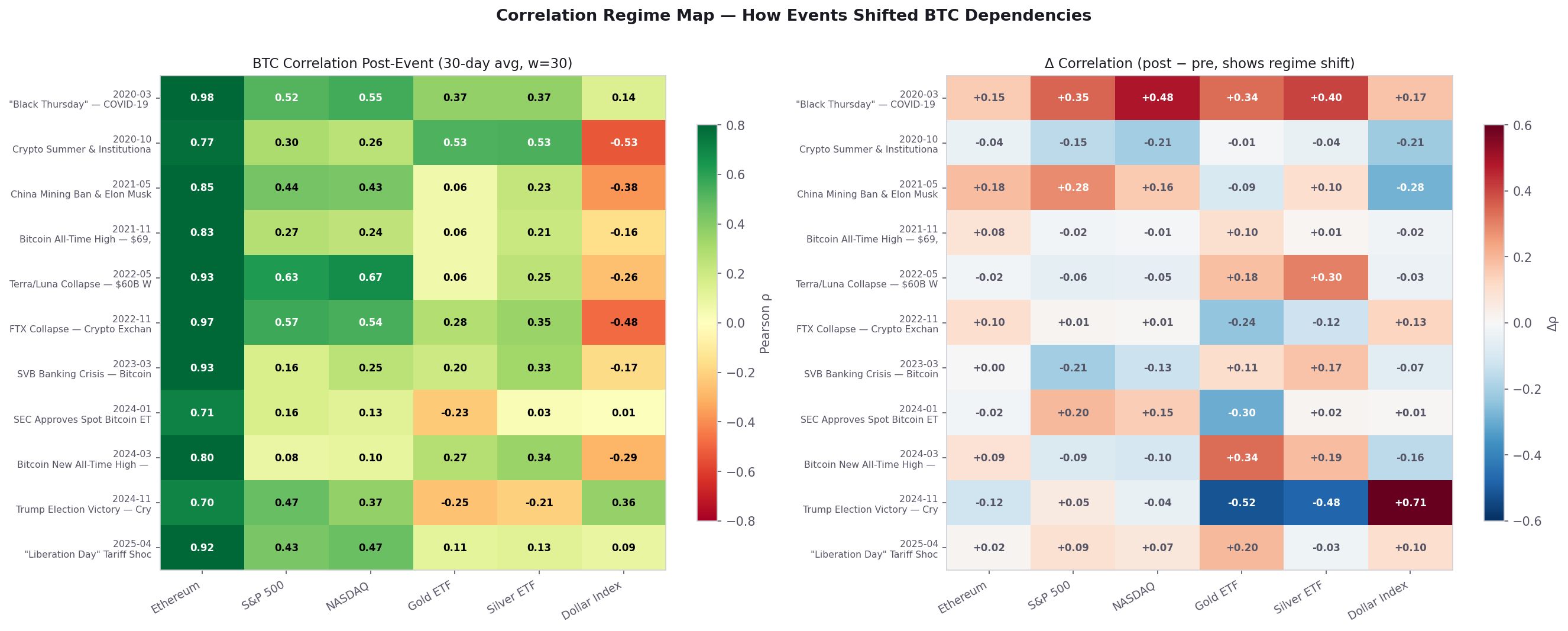

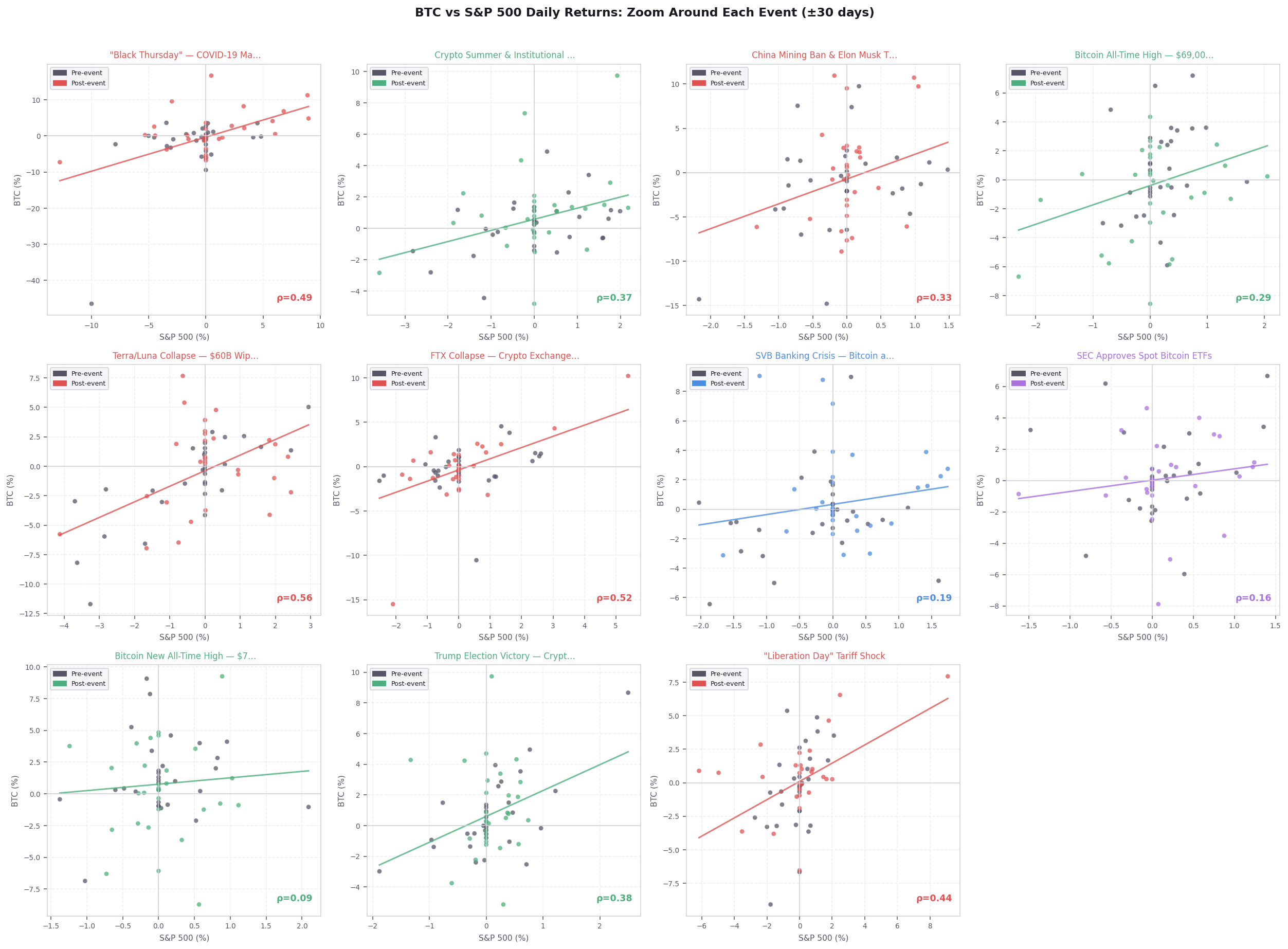

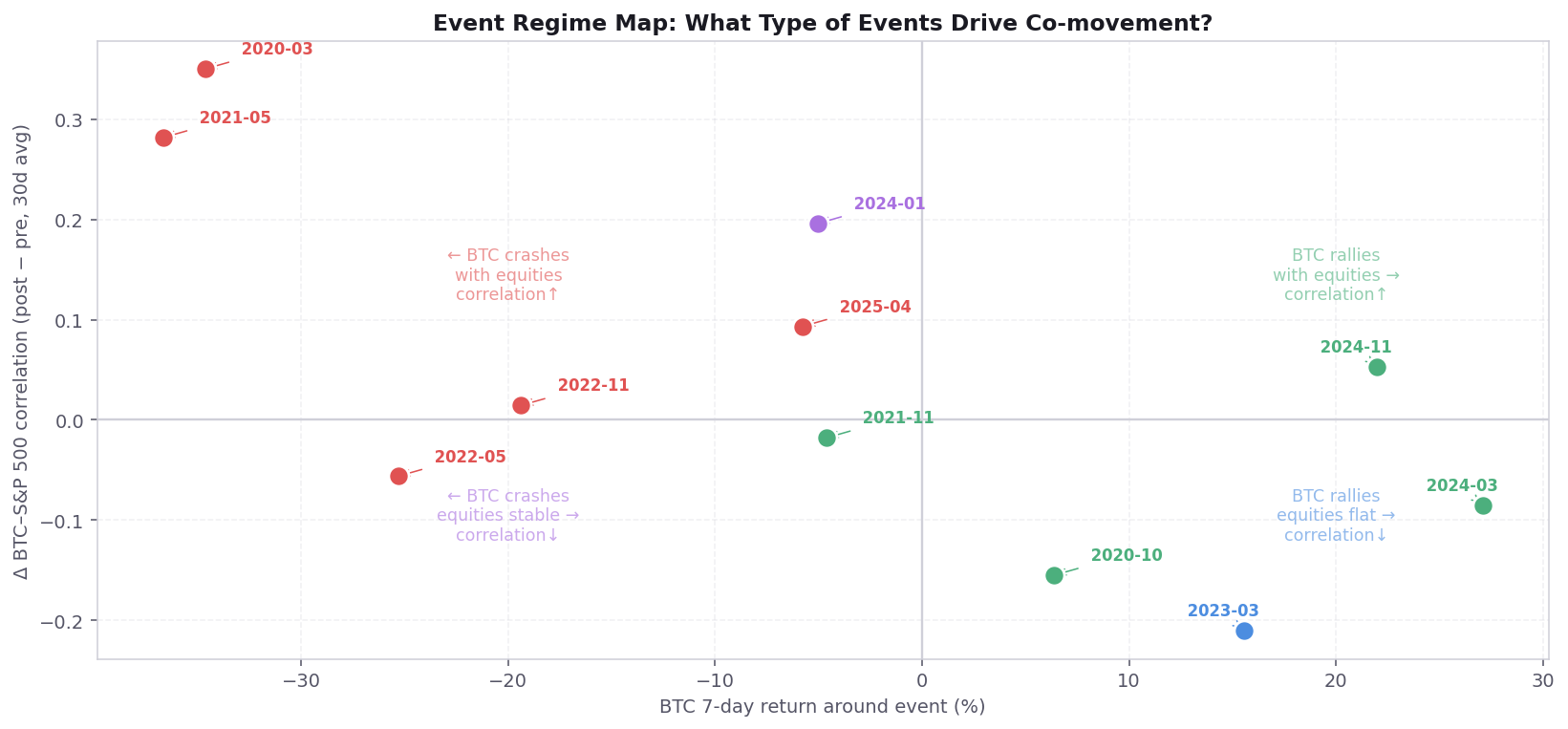

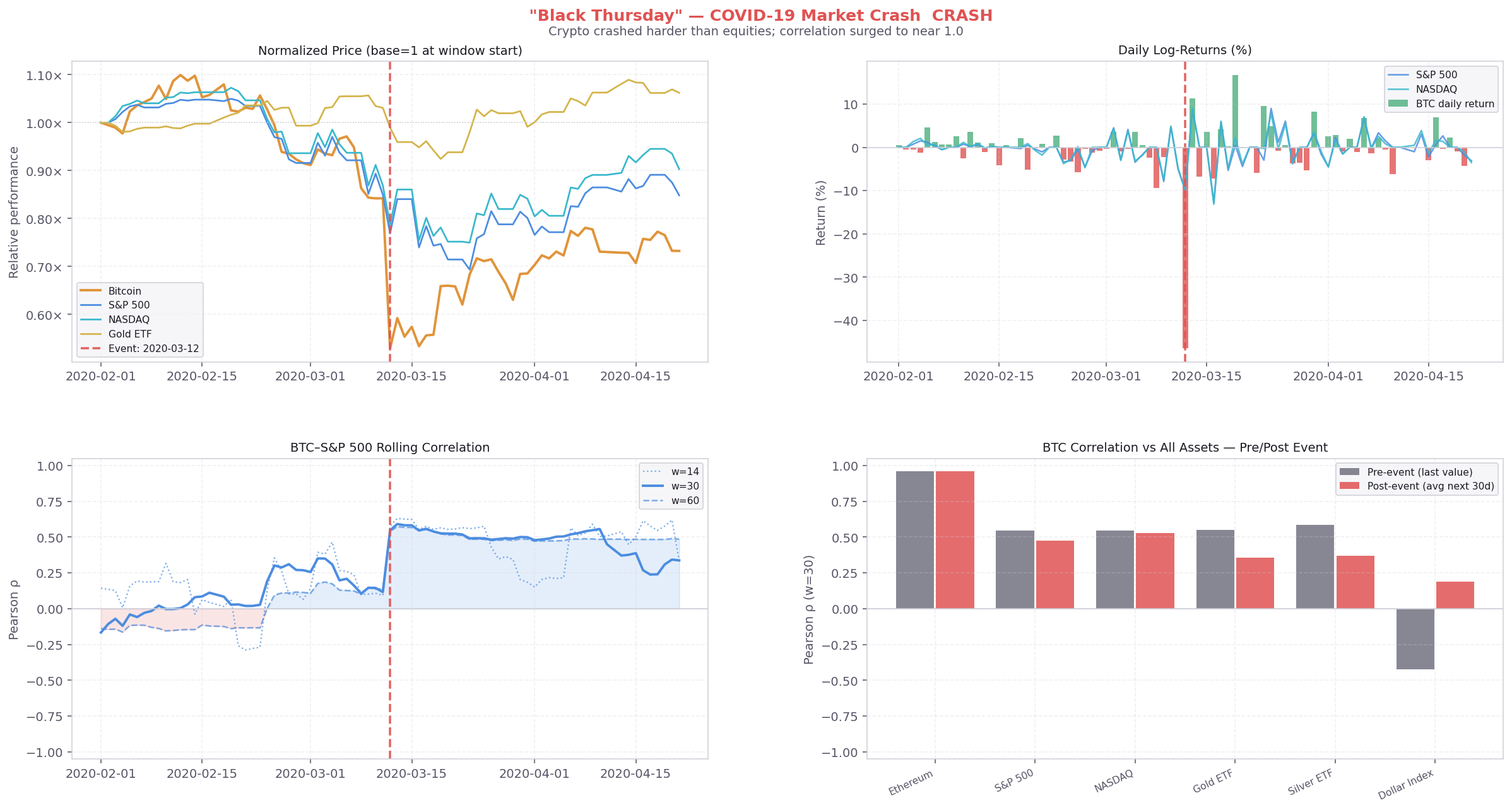

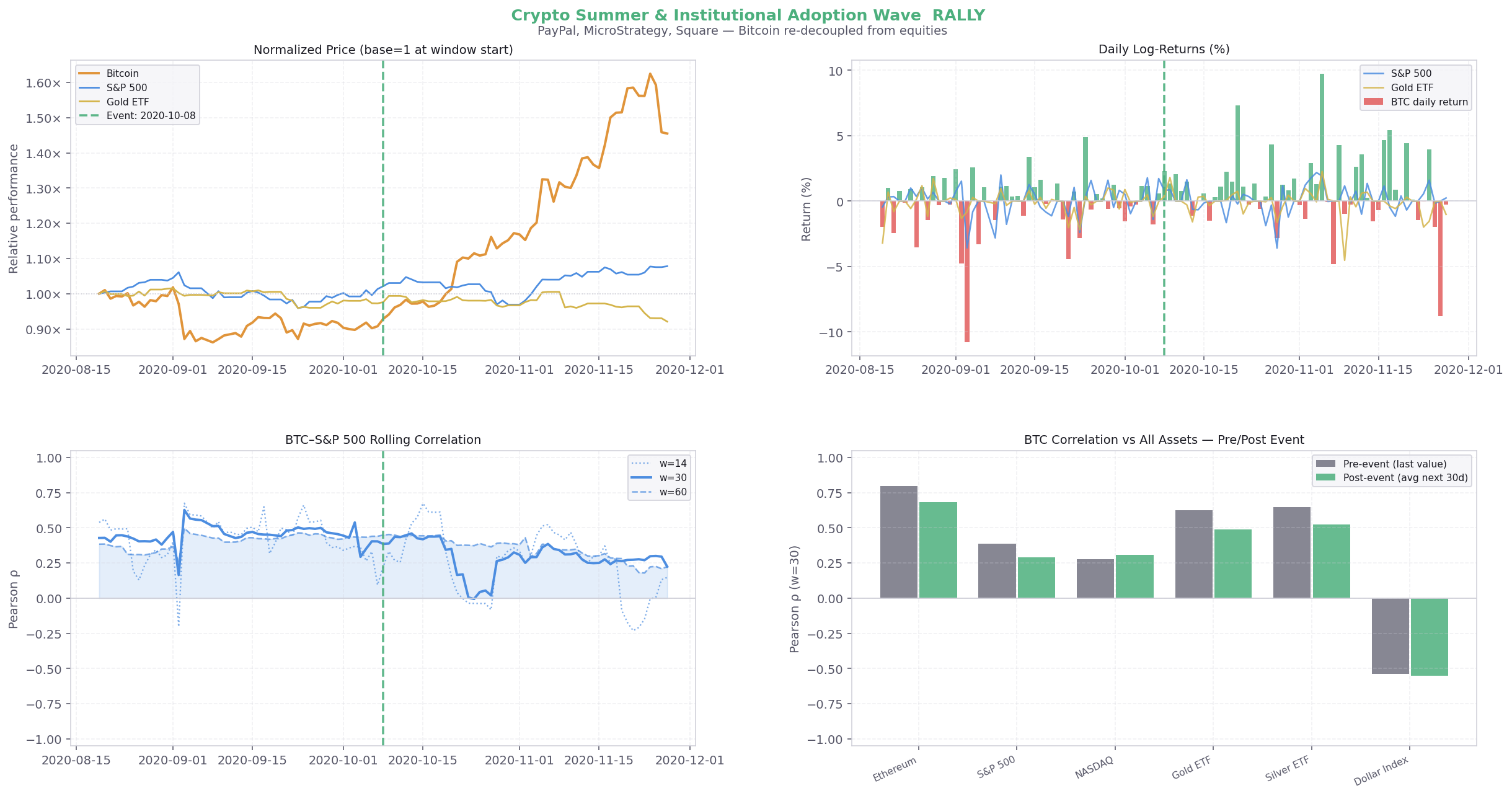

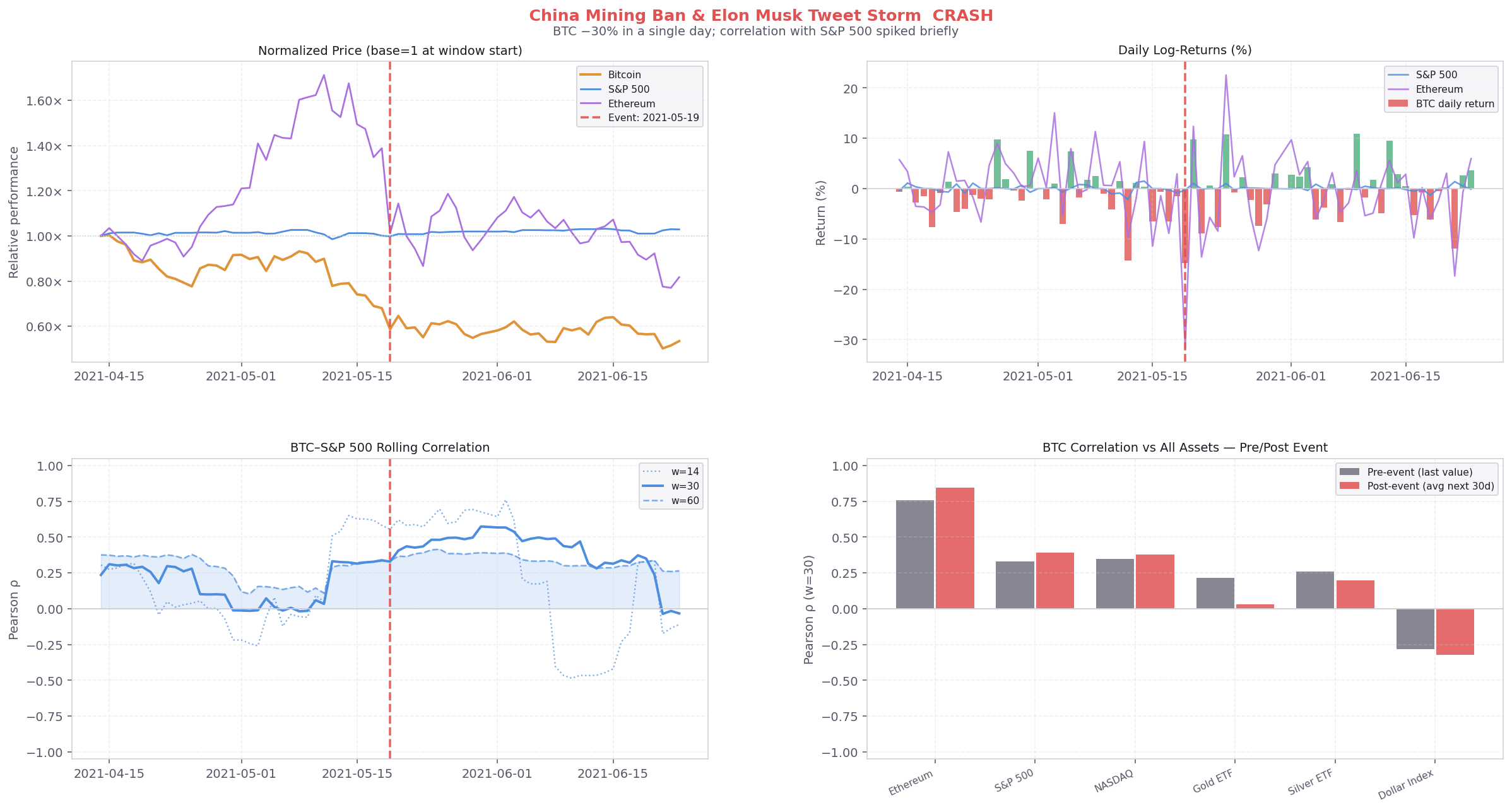

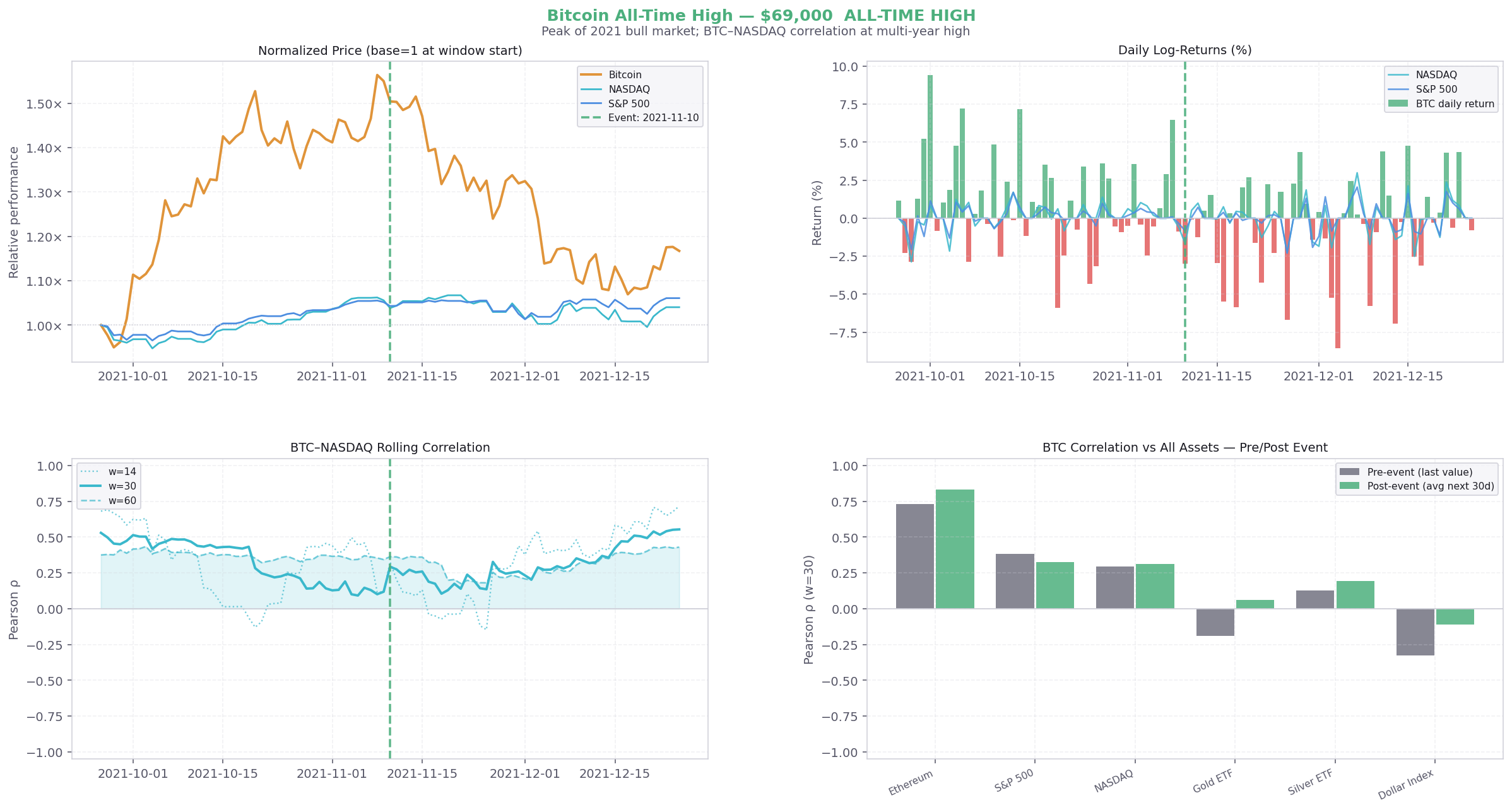

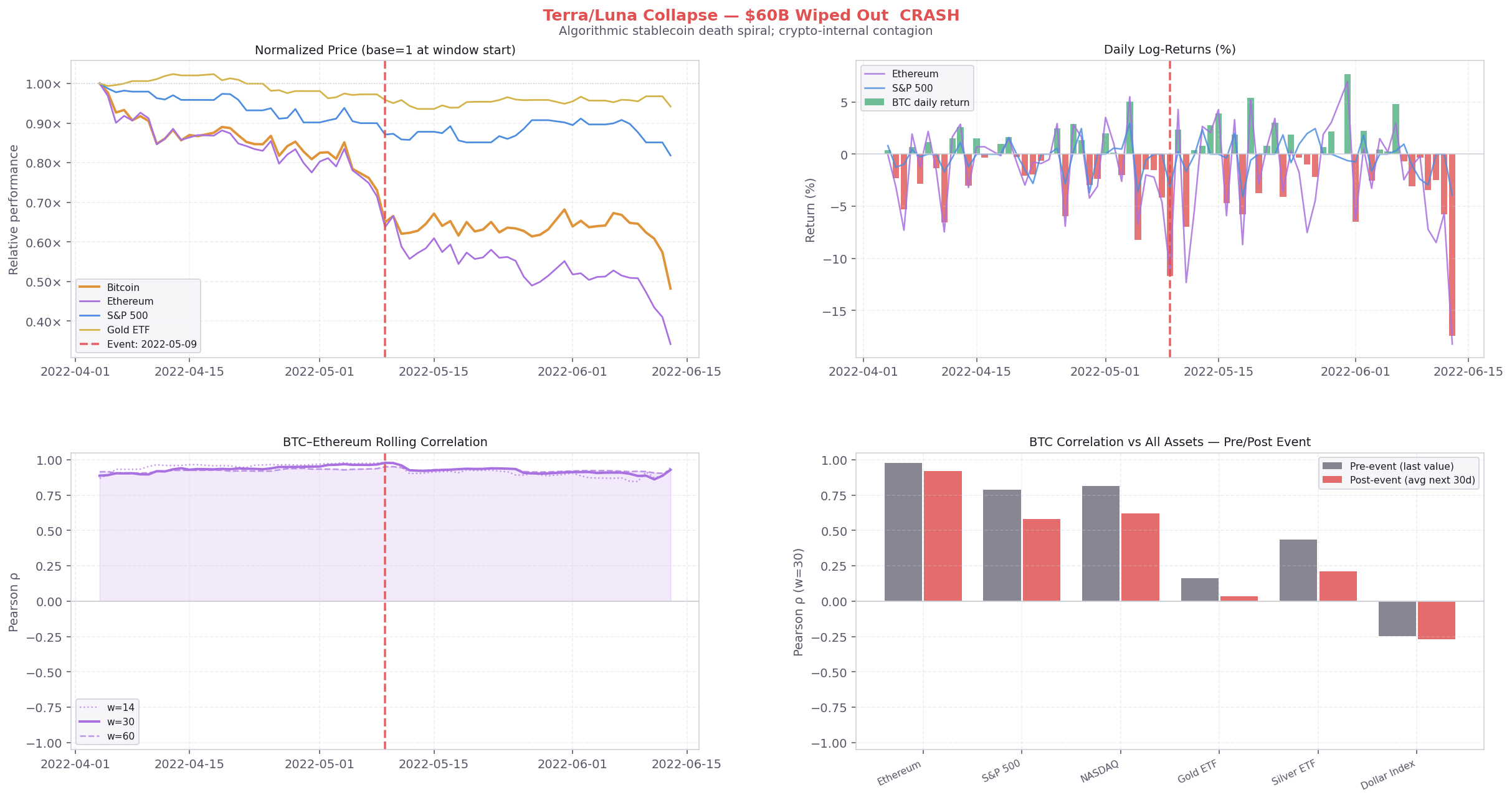

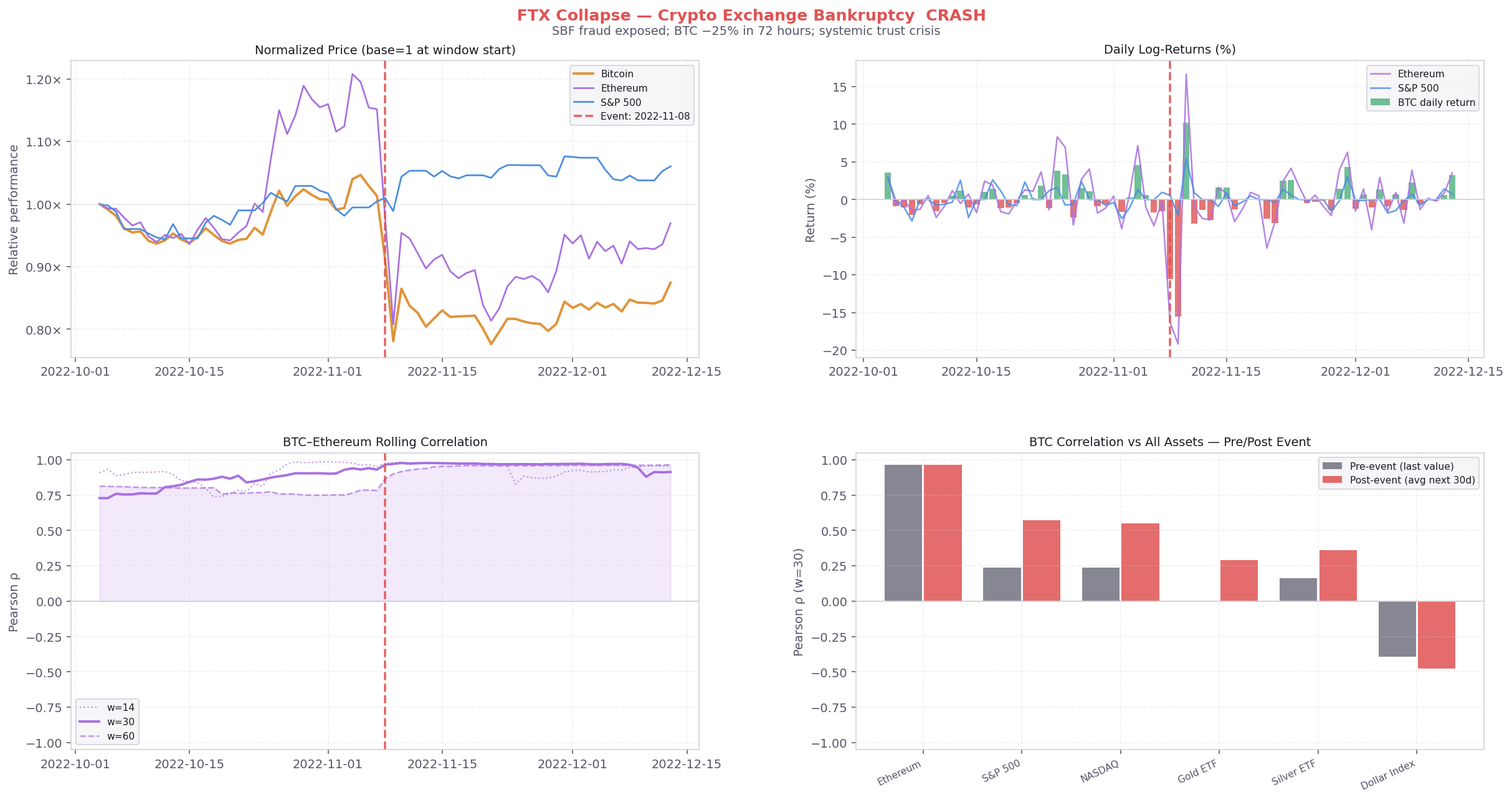

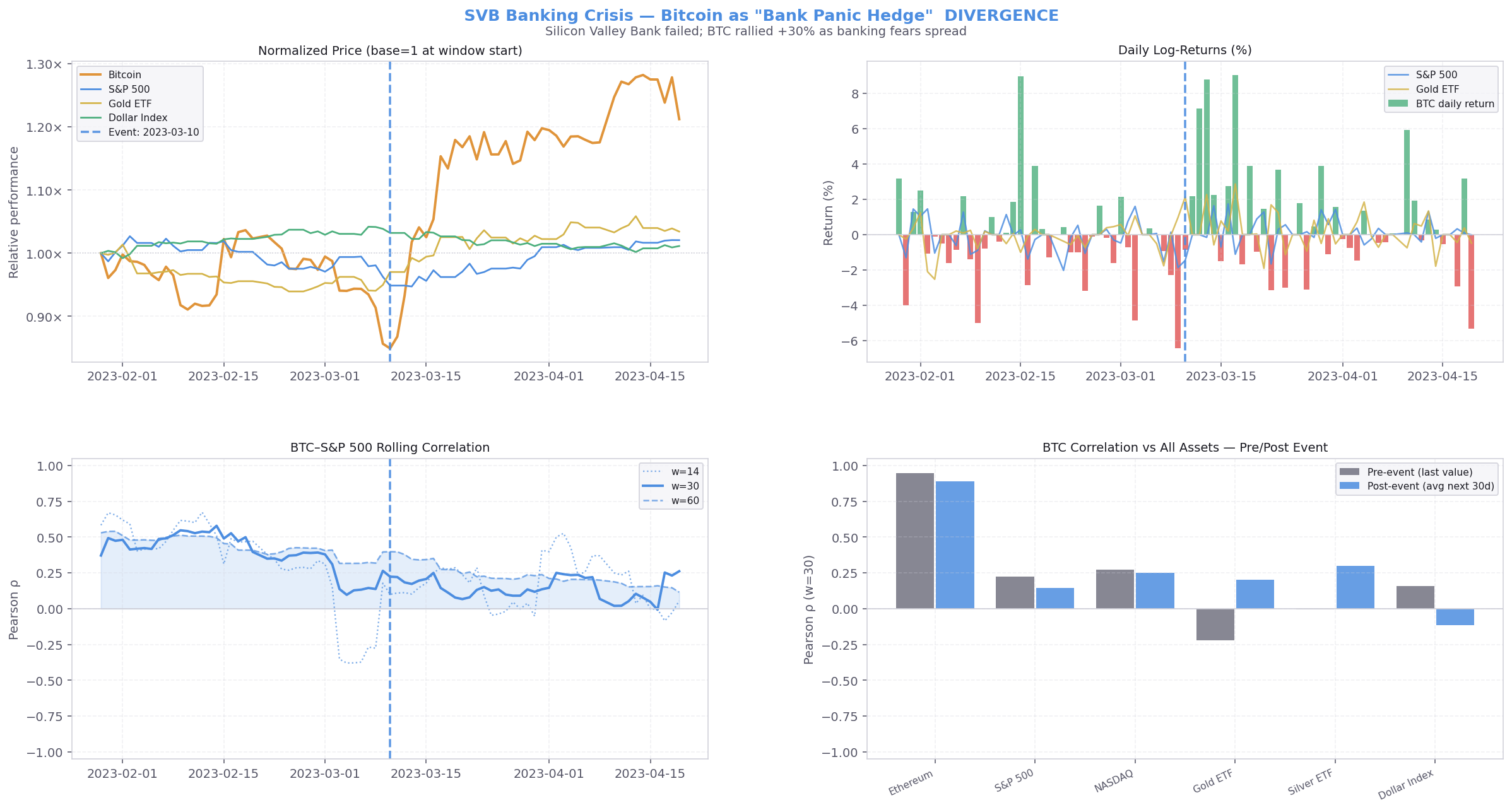

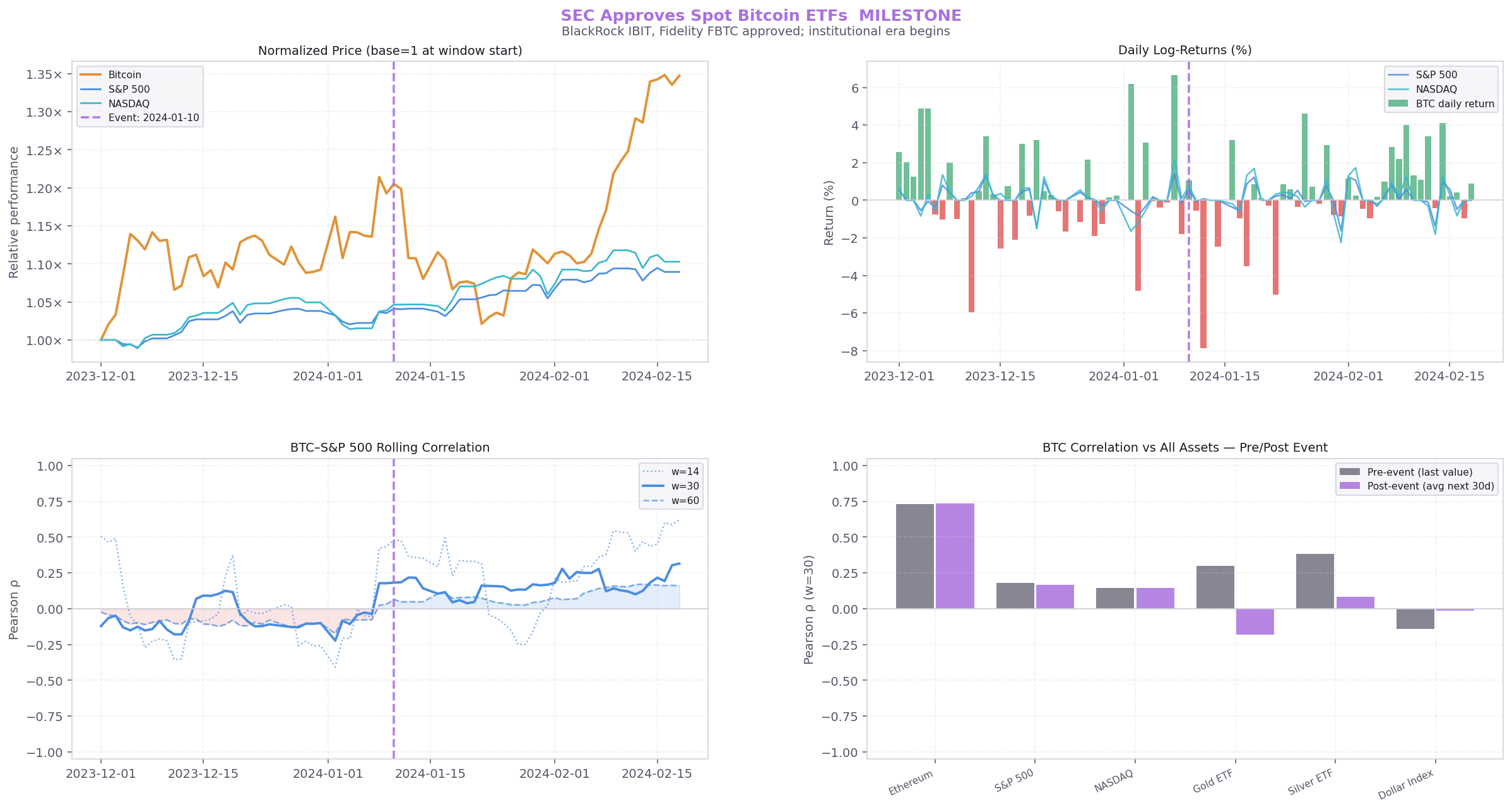

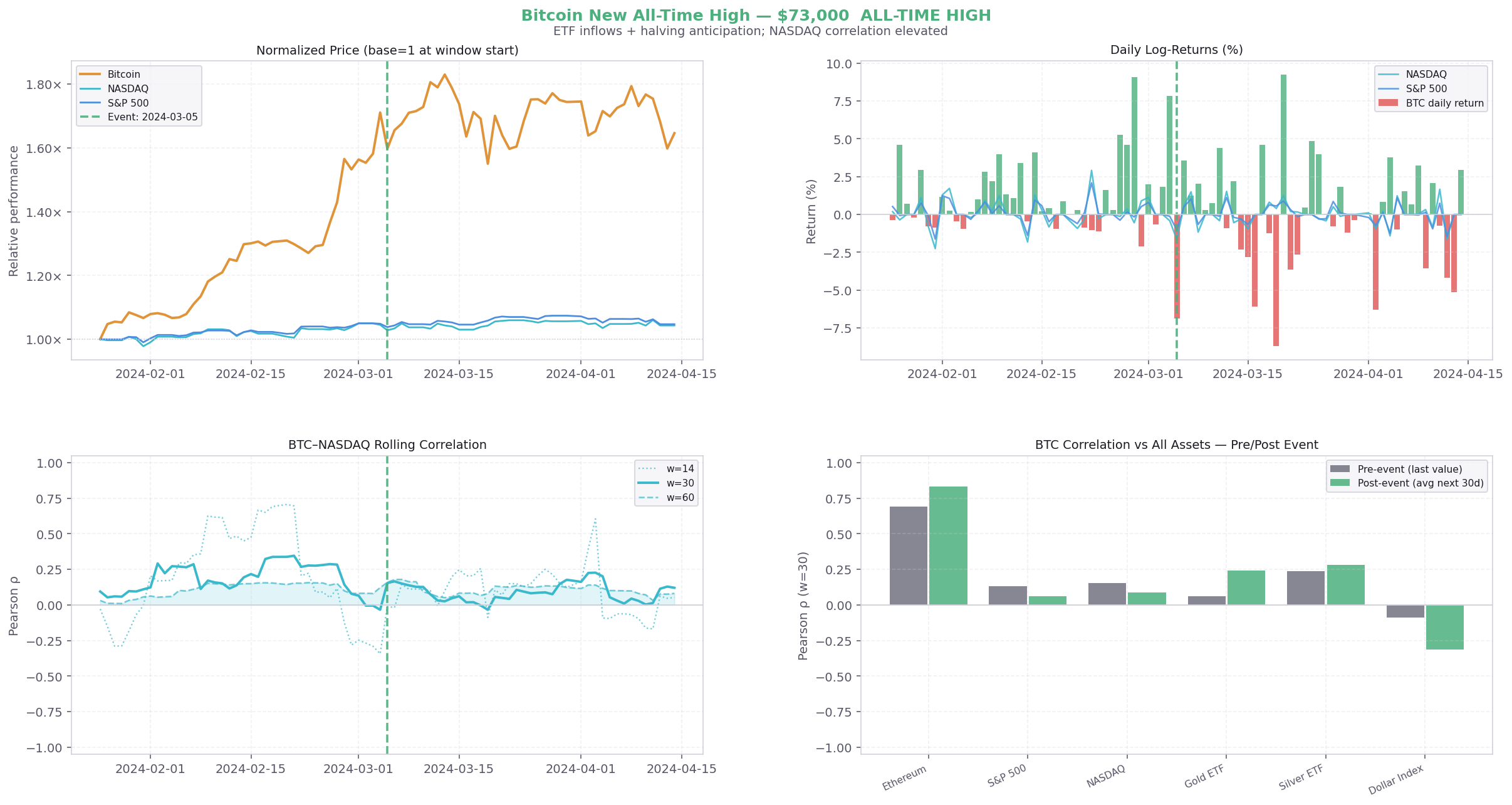

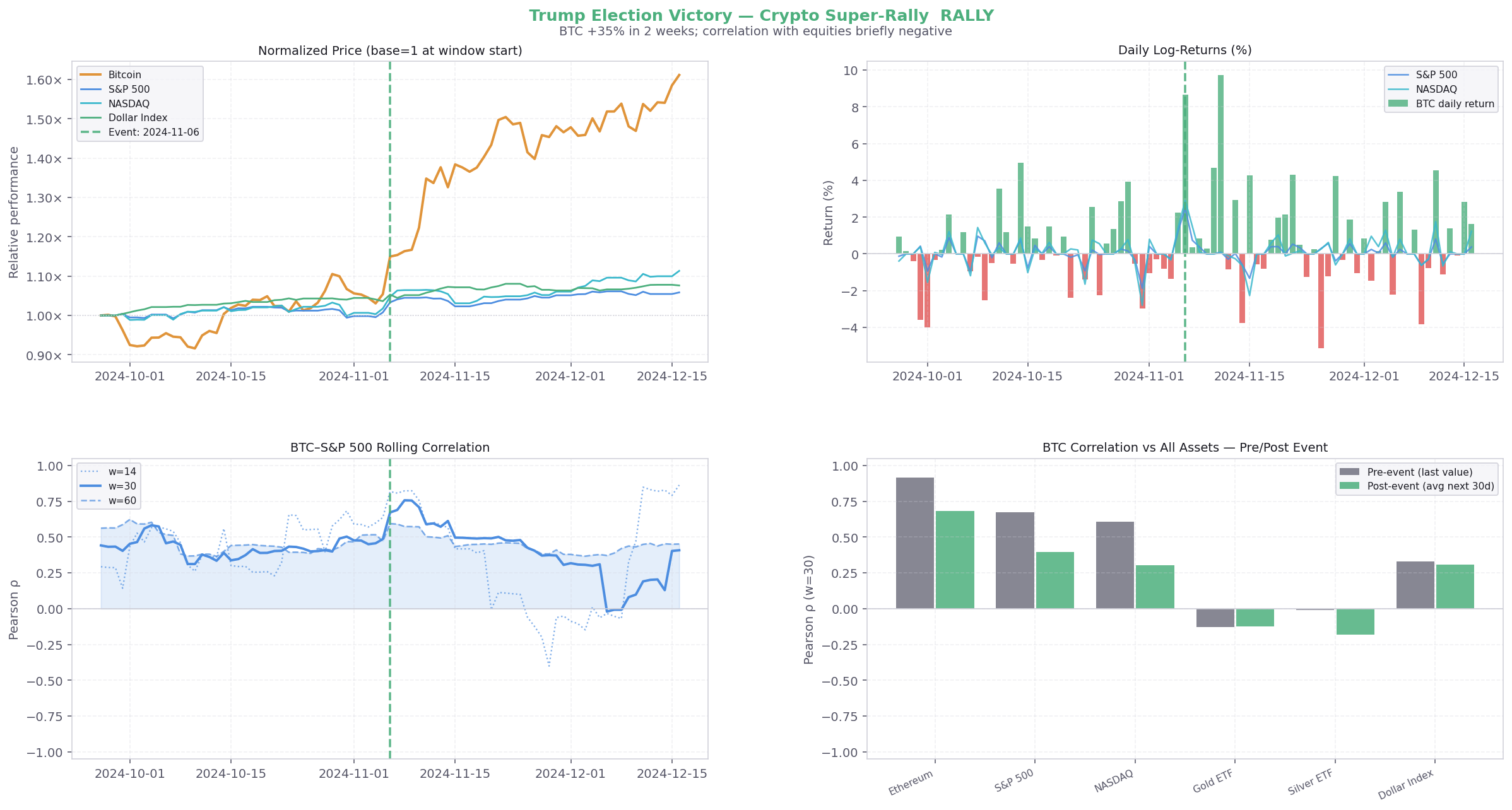

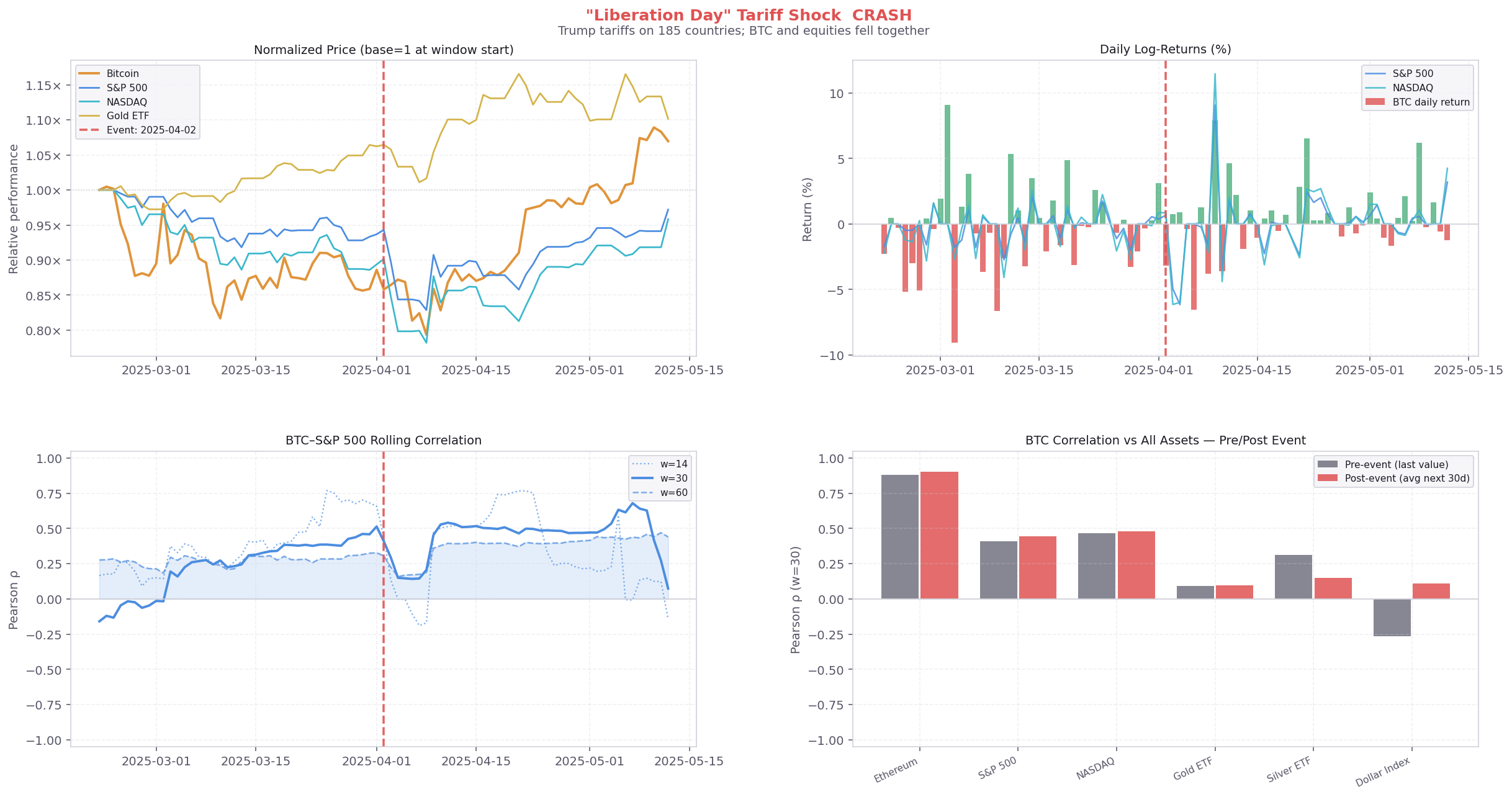

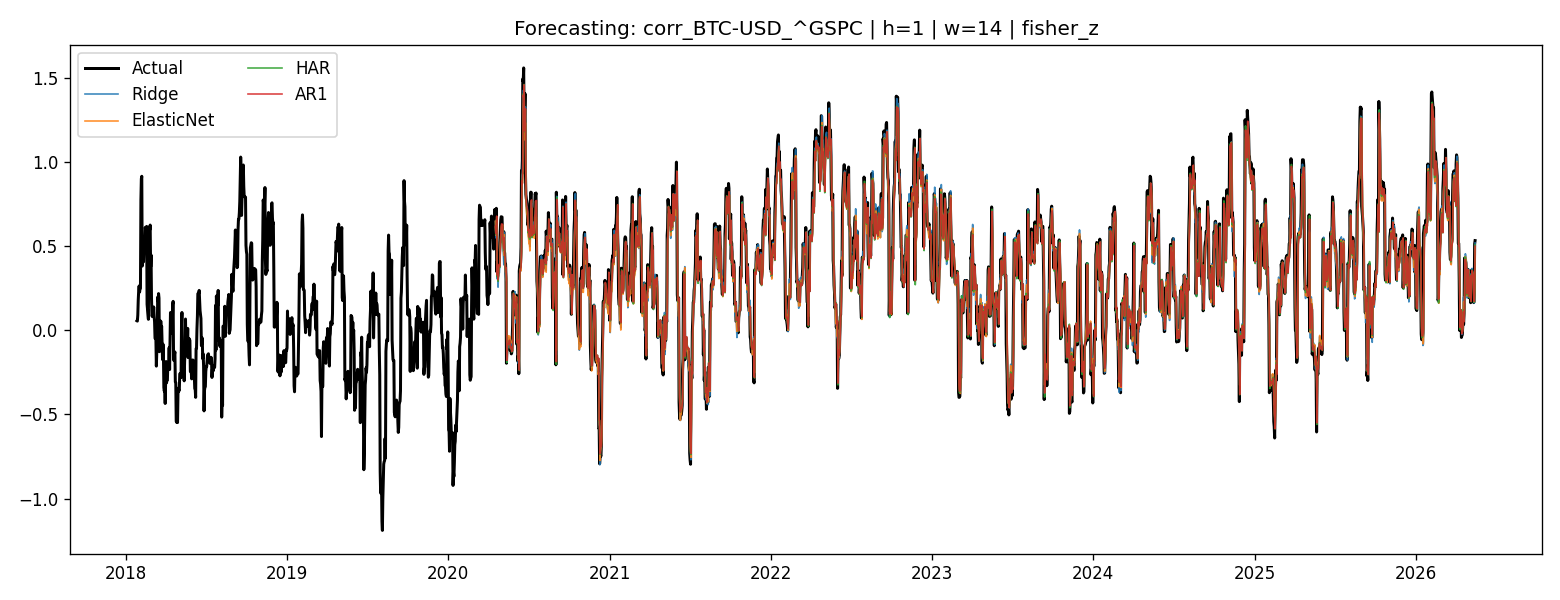

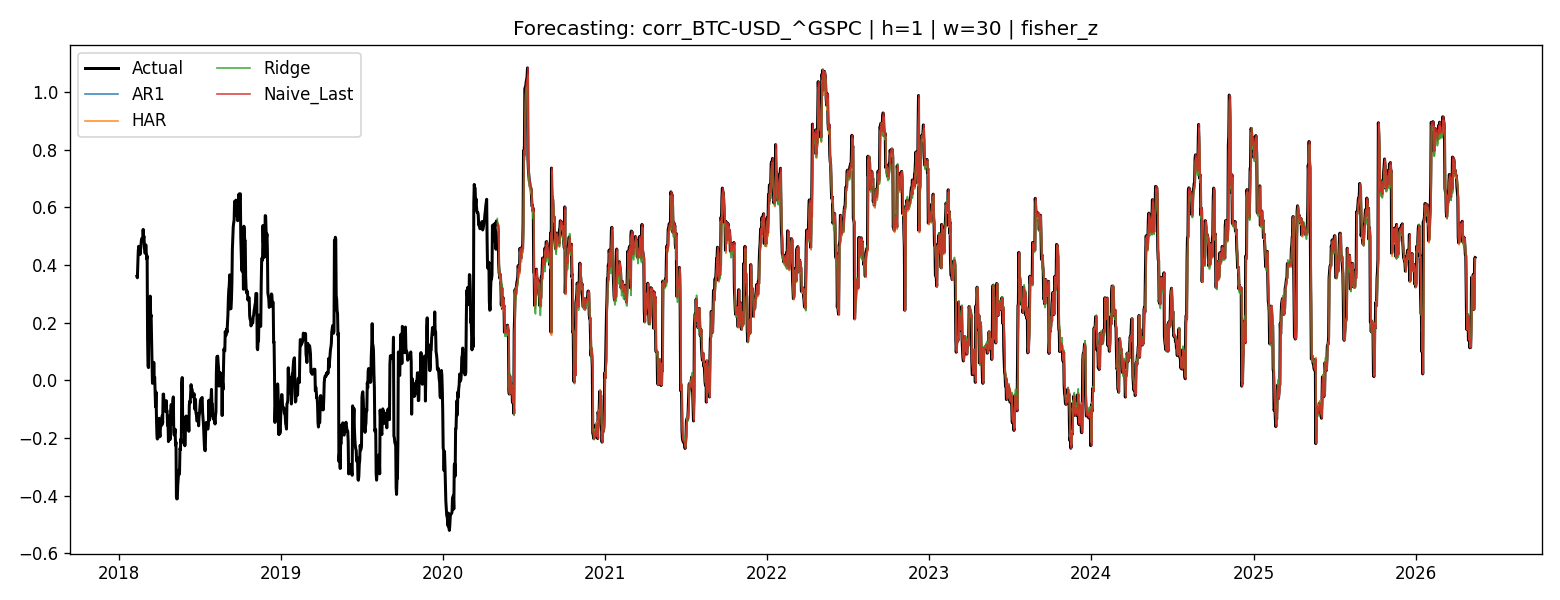

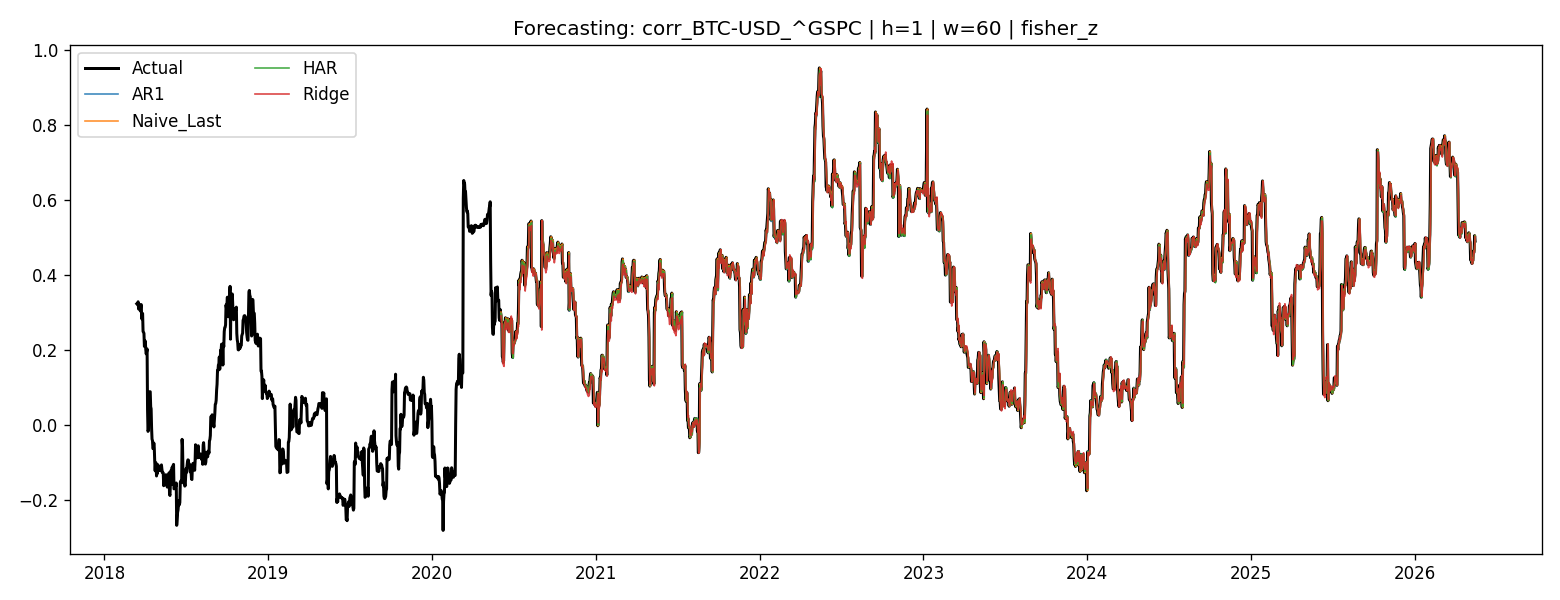

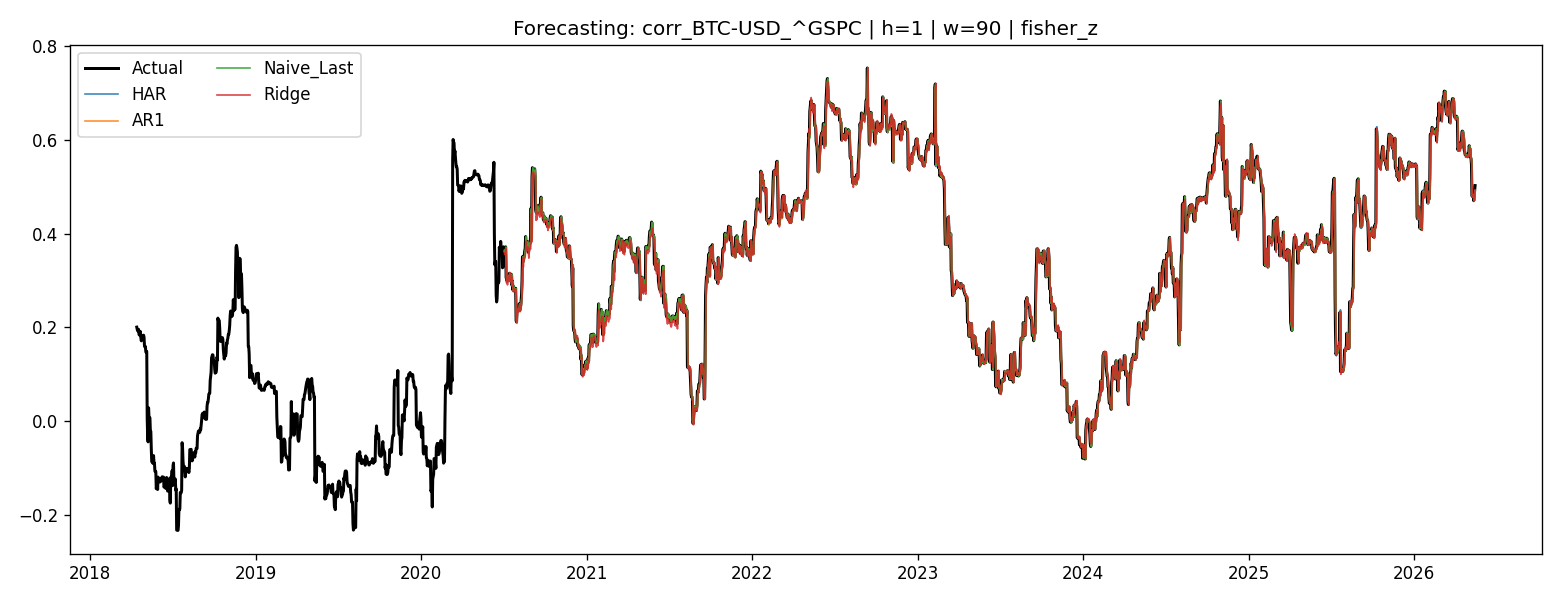

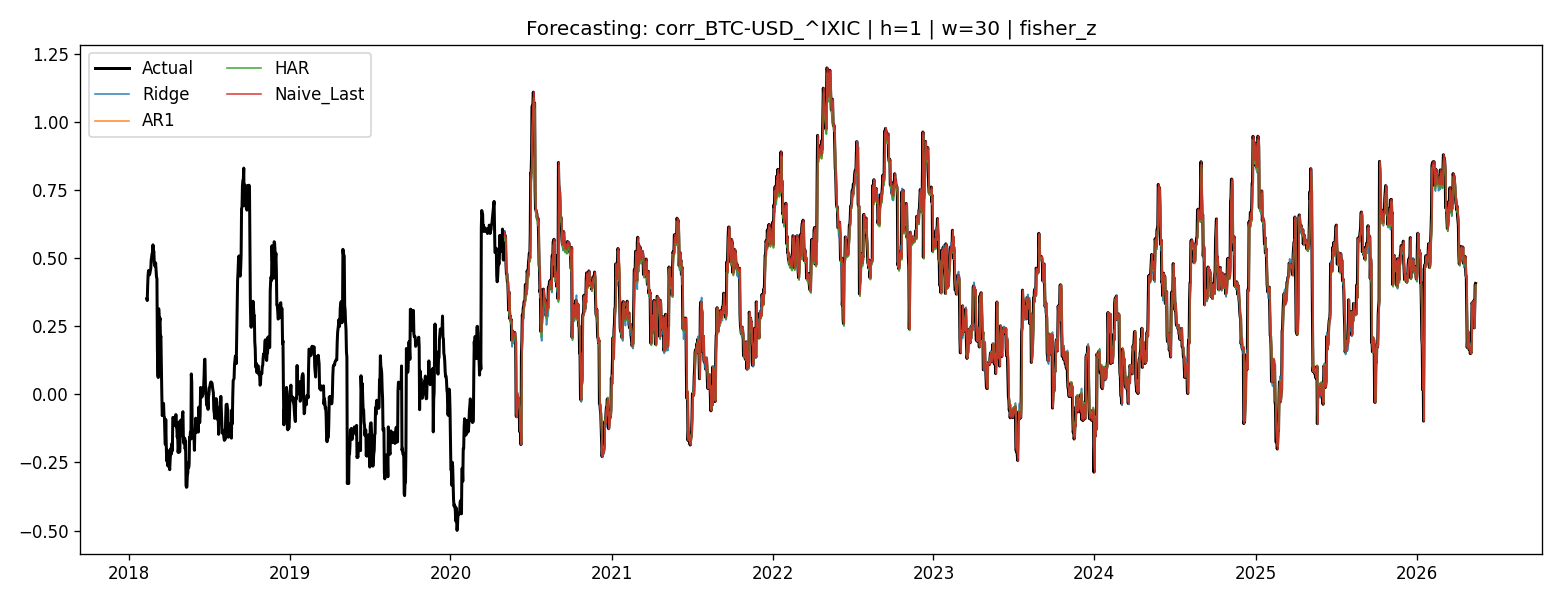

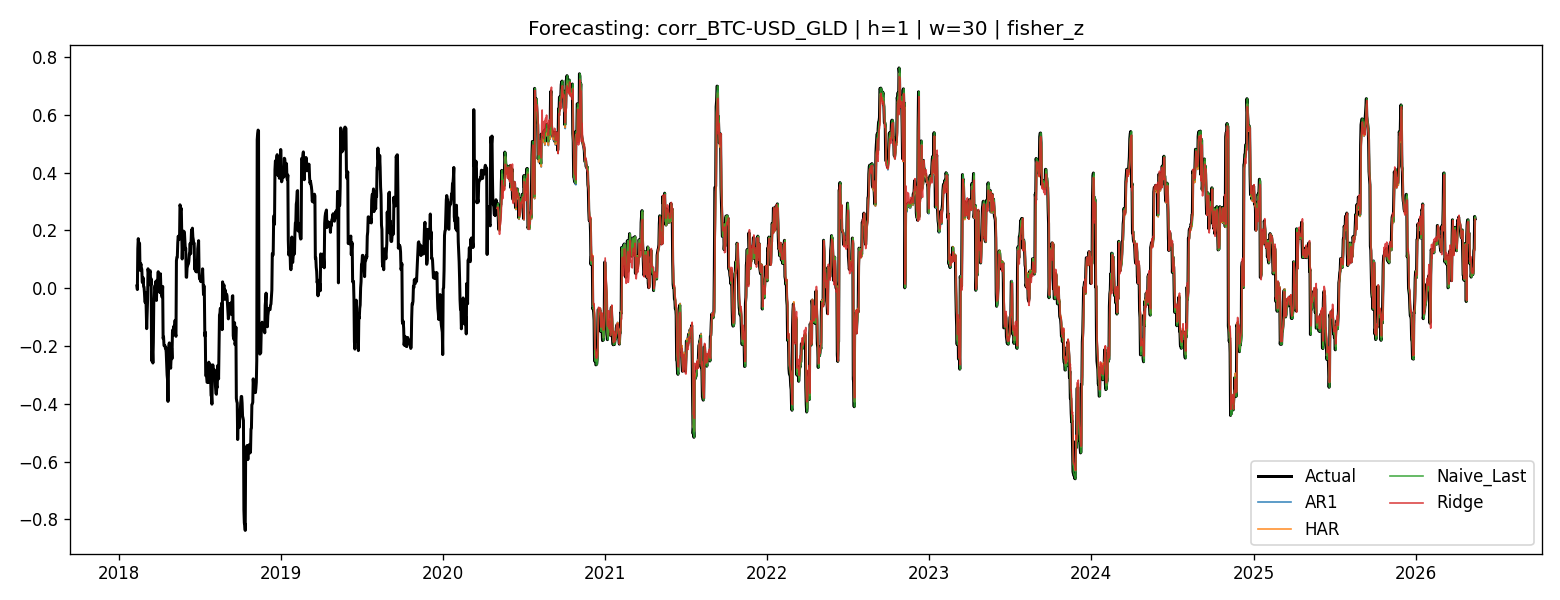

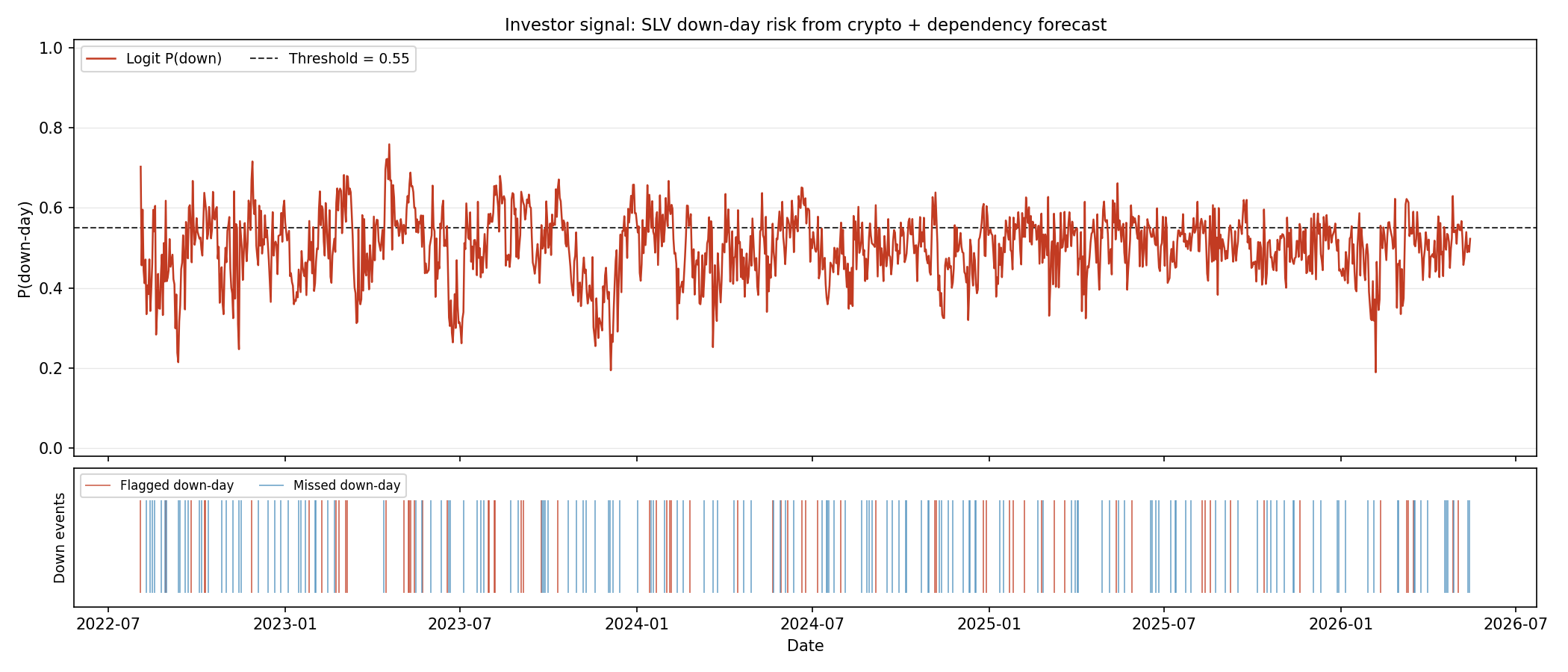

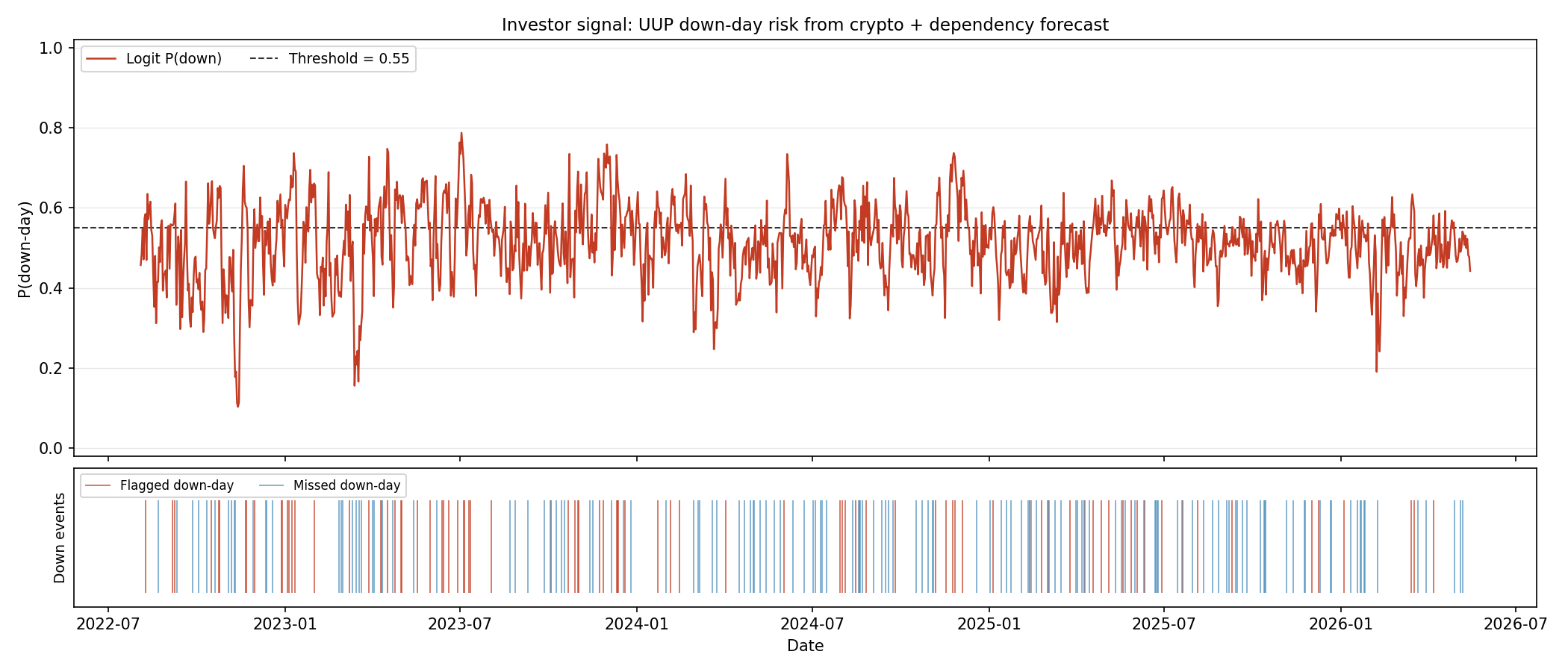

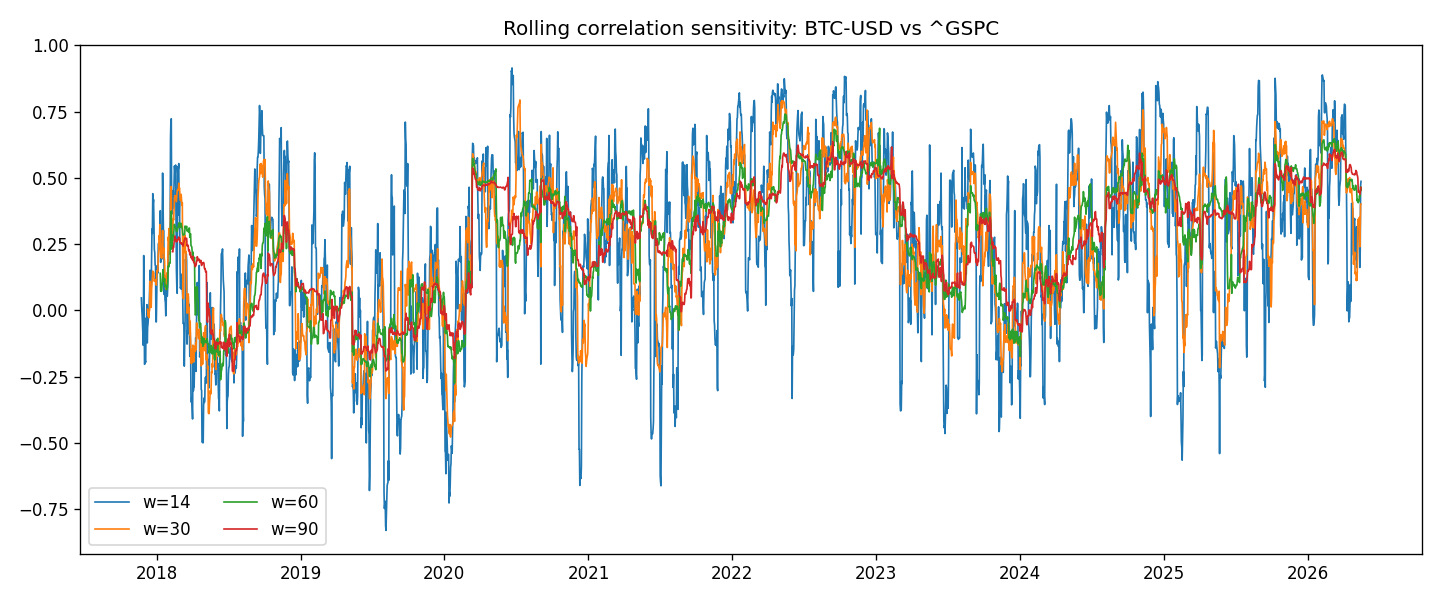

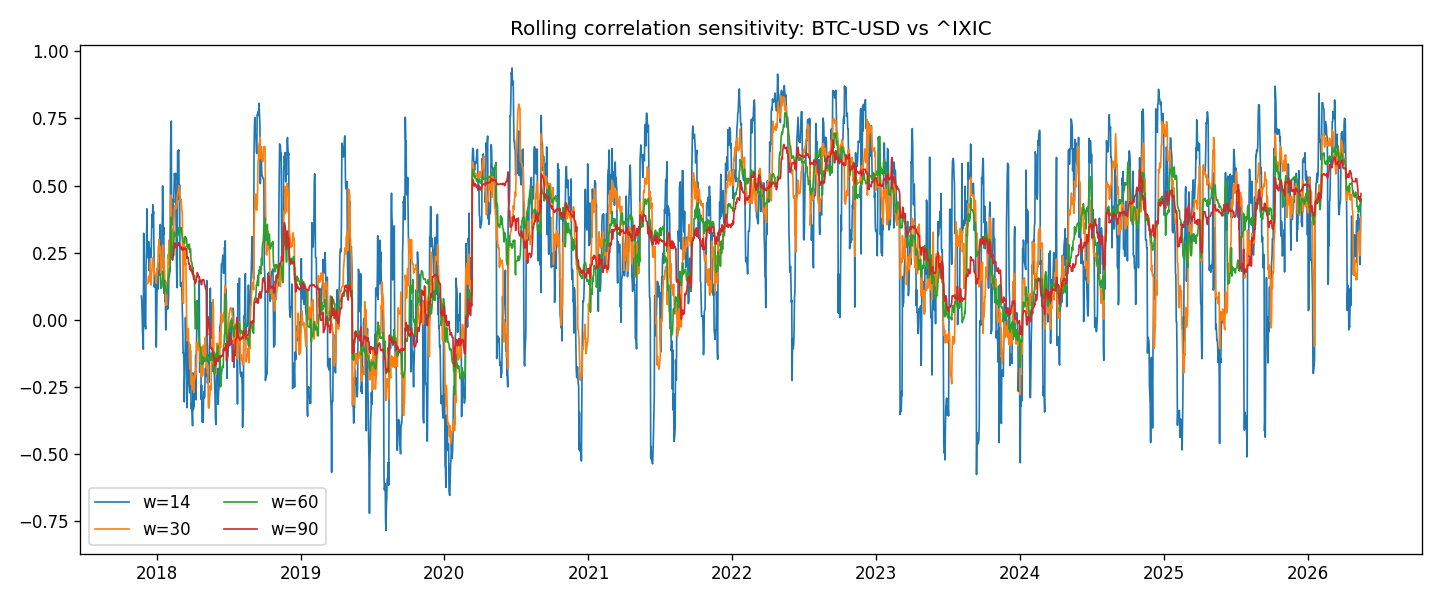

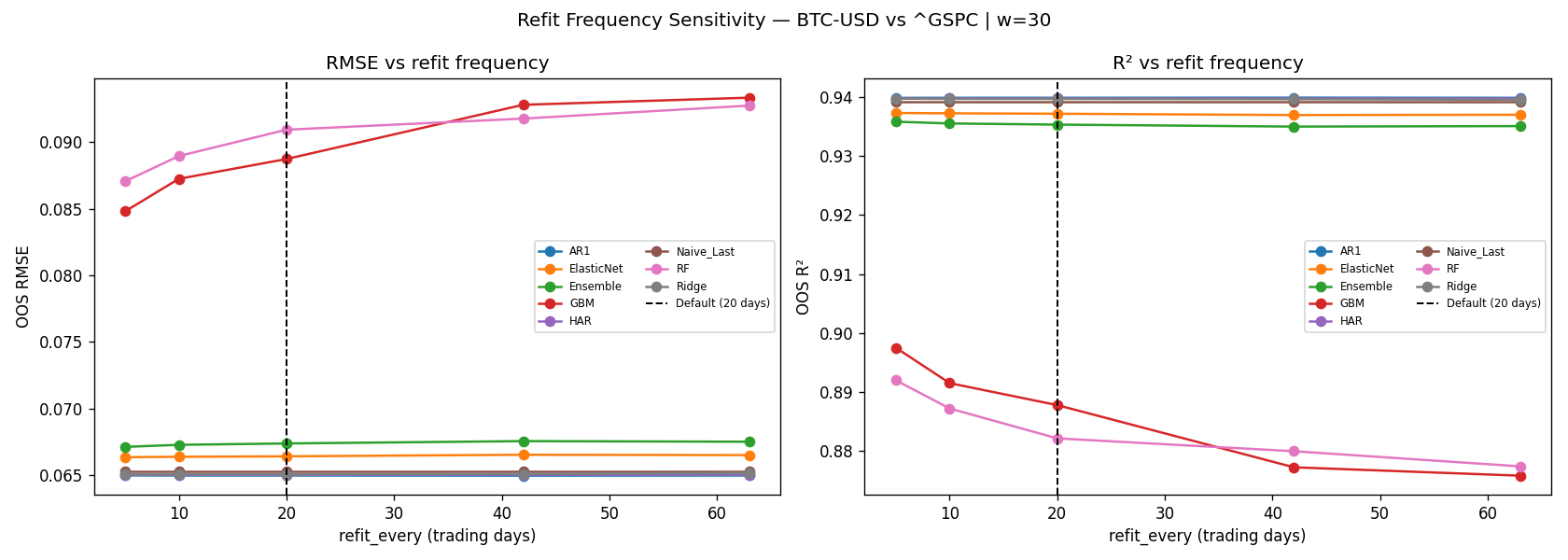

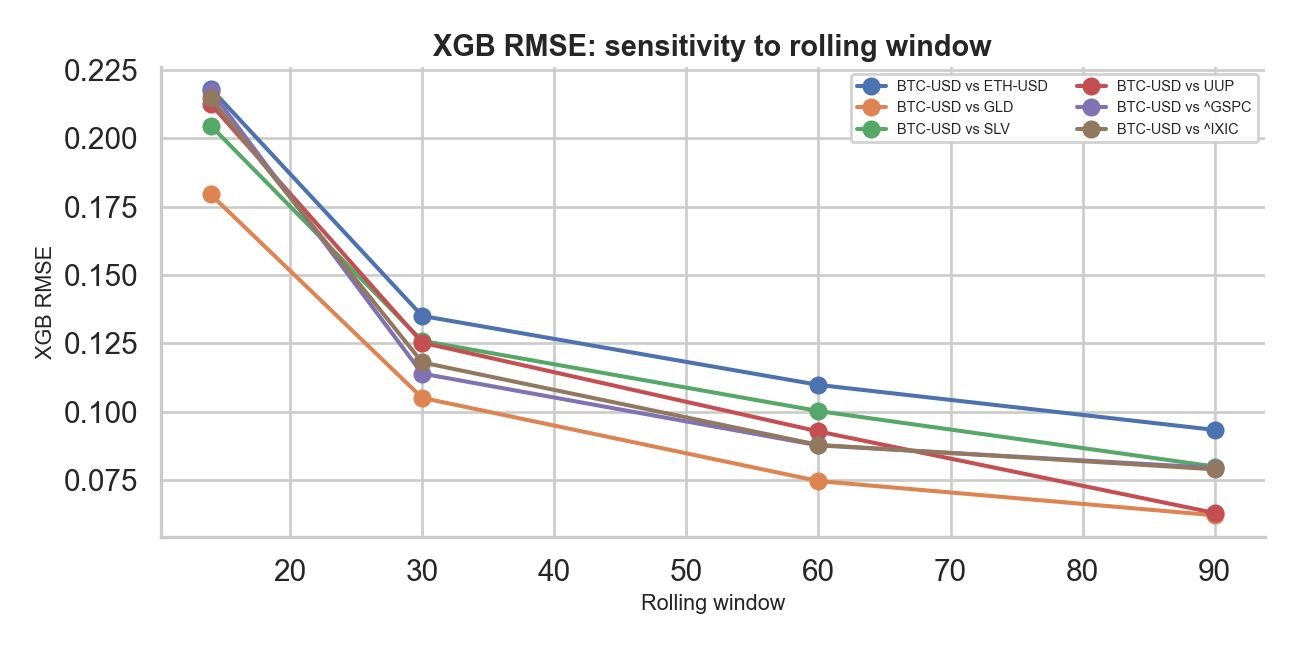

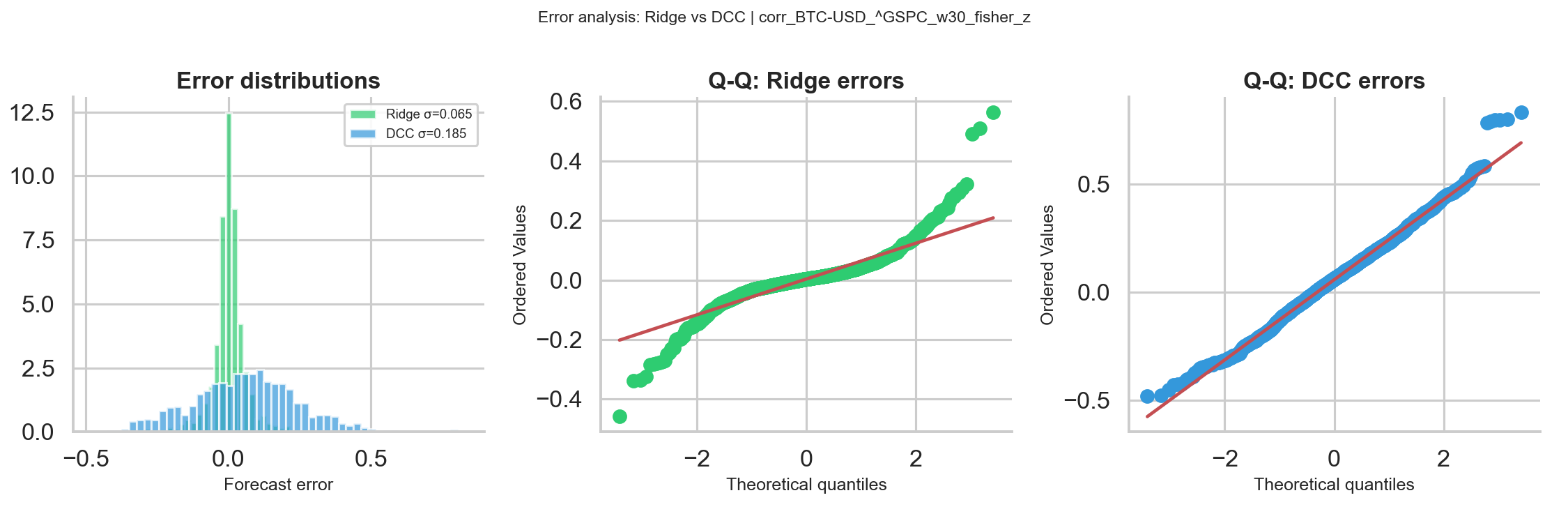

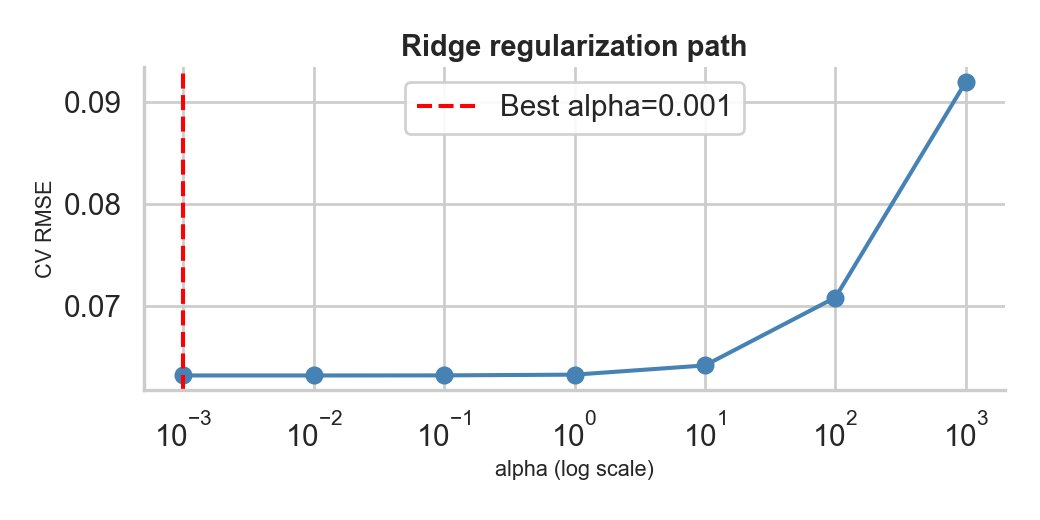

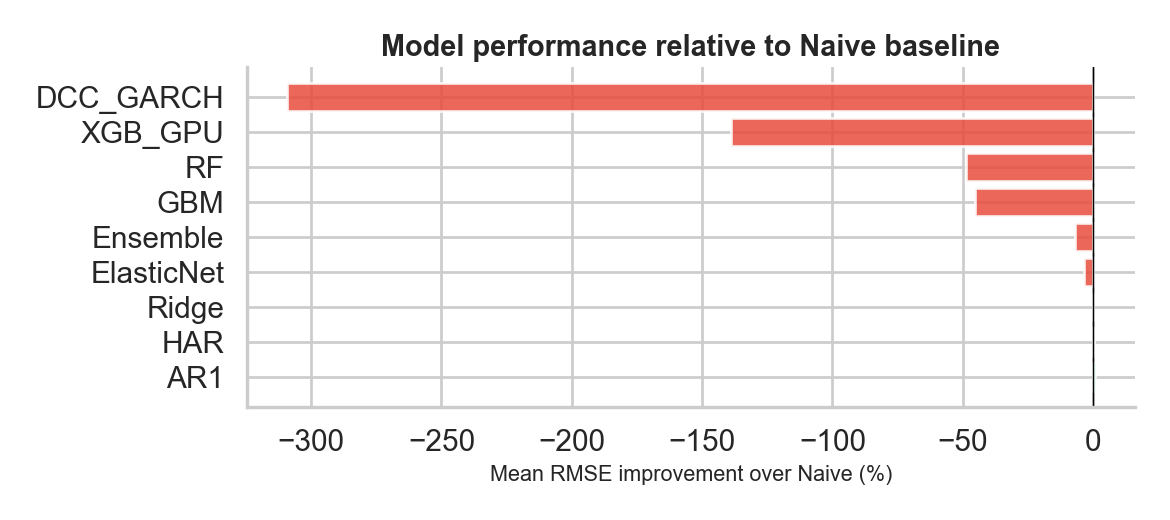

Exploratory Figures